Getting the overall data from Baker Hughes the rig count can be plotted, over time, to give the following:

Figure 1. Rig Counts in the Middle East (Baker Hughes)

If one looks at the trend for the last twelve months, it has remains on a fairly consistent upward trend, following that of the longer time interval plot of Figure 1.

Figure 2. Recent trend in Middle East Rig count (Baker Hughes)

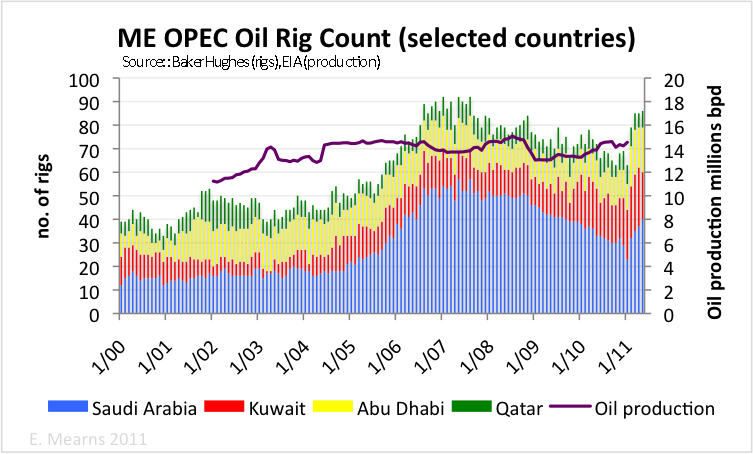

Back in the days of The Oil Drum, Euan Mearns and I had this concern, which occasionally surfaced, about these numbers. From my early post on the subject which noted that back in 2005 the KSA were running around 20 rigs, which would not be enough to get them the production they were claiming to need in the future, to Euan’s in 2011, the topic was revisited regularly over the time that the count steadily mounted as the Kingdom had to drill an increasing number of wells just to keep production at around the same overall level.

I am using the KSA as the example, given the large volume of its production relative to that of the others in the Middle East, but as the numbers show, the trend toward increased drilling rate to create enough productive wells to sustain production as the larger volume wells dry up is starting to become a steadily more frantic race across the region.

Rune Likvern used the phrase “Red Queen” in discussing the overall long-term need of the companies in the Bakken to have to drill an increasing number of wells, with individually reducing production, in order to remain in place with regard to overall production. As the production from the Bakken now exceeds a million barrels a day it may seem foolish to be predicting this “squirrel cage” view of the future, but the rig count up there is still running at around 190 rigs, which is not enough to sustain future growth for long, given that access to the sweet spots is limited, and they are beginning to run out of new sites.

So it is in the Middle East. The rig count numbers are mounting steadily, it is reported that there were 88 rigs drilling in the country in October 2012. Last year this rose to 170, and the number is expected to rise to 210 by the end of this year.

Aramco have done remarkably well, over the past decade, in developing new technologies to harvest the attic oil left around the tops of the major producing formations such as Ghawar, as the main body of the fields begin to be exhausted. But the problem with these secondary rig operations is that they were directed at the smaller pools around the field, rather than tapping into the major volume, and thus they had an expected and finite life. That life is starting to come to a close. Just as, when sucking a thick milk shake through a single immovable straw, when it stops drawing fluid, there is still a fair amount left in the cup. But as you move the straw around and slide it up and down the sides, the amount that you recover gets less, and it takes greater and greater effort to get it, to the point where you quit and discard the carton. And that is where the Middle Eastern oilfields are beginning to find themselves.

The high-quality light oils of the mainland are rapidly running out, and the remaining fields with the promise for sustaining Saudi production at around 10 mbd for the next few years, are the heavier sour crudes from the offshore fields such as Safaniya and Manifa. At the same time there is a need to reduce the increasing amount of oil (now at 3 mbd) being consumed in country, with the hope that this can be replaced by domestic natural gas. But those hopes are being reduced as the shales are found to be less productive than anticipated, and hopes are now switching to the slower production that can, hopefully, be achieved from the tight sands – but at the cost of an increased number of wells, inter alia.

This is the writing on the wall for global oil production, and in the short-term it will be neglected. Increasing the number of rigs will, in that interval, increase the number of wells that will produce, even though the volume from each well will be less, and the overall life of the wells will similarly reduce, as higher production techniques tap into smaller fields.

But we are now on the treadmill in the squirrel cage, or, as Rune would have it, we have wrapped ourselves in the cape and crown of the Red Queen, and must run faster and faster just to stay in place. (There are additional concerns since, as an example, Manifa could not be brought on line until there were refineries built that could process that crude, and so the options for increasing production beyond the capacity of refineries to absorb that increase is a futile exercise).

There will soon come a time when the gain from the overall increase in new wells will not match the decline in production from older wells, particularly if the effort to “run faster” is restricted to only a few players (Russia for example is not yet putting the effort and investment into increased drilling rates in order to sustain their overall levels of production, and given the age of their major fields are likely now in terminal decline).

Ouch!

{kind=link}