We project that by 2035 the US will be energy self-sufficient while maintaining its position as the world’s top liquids and natural gas producer.This illustrates the optimism which BP are projecting in their image of future production. But it carries with it a lot of inherent assumptions, some of which are relatively easy to identify in the summary graphic presentation that accompanied the initial presentation of the new report. Perhaps the most illustrative of their optimism is this plot, which shows the increasingly decoupled changes in energy supply relative to projected increases in GDP.

Figure 1. The reducing dependence on Energy growth as a control on GDP. (All figures are from the new BP Energy Outlook for 2035)

Each year there are significant projections for the future of energy over the next few decades. Recent posts have reviewed this year’s projections from the IEA and ExxonMobil. These projections, were also reviewed last year and those reviews included the previous BP projection although that only projected forward to 2030 – the current review has added five years to this.

The relative contributions of the different fuel sources to the overall mix have not changed appreciably in the past year. Oil is anticipated to continue to shrink in percentage contribution, and coal will also decline in relative contribution after around 2020. Natural gas and renewables are anticipated to make up the supply needed.

Figure 2. Relative contributions of the different fuel sources to overall global energy supply to 2035.

BP have made it a little easier to see how this breaks down by plotting the ten-year increments in fuel contribution as well as the overall totals.

Figure 3. Changes in projected fuel supplies over the period to 2035.

Changing the plot to show the ten-year incremental changes illustrates how coal, now surging as an international fuel source, is anticipated to decline beyond 2020.

Figure 4. Projected ten-year incremental changes in fuel supply through 2035.

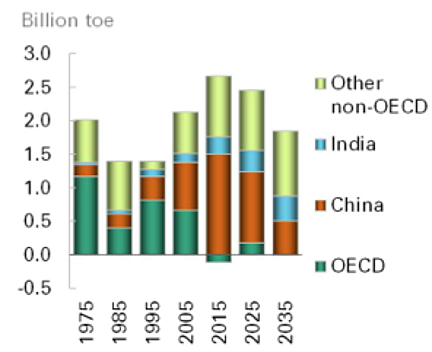

Note that in overall total BP is projecting that global consumption will rise by 41% over today’s numbers, most of which increase will come from the rapidly-developing countries of the world.

Figure 5. Regional increments of energy consumption growth over the decades to 2035.

The reliance on the improvements in energy efficiency to stall further growth in energy demand from the OECD countries is evident in this picture.

BP notes that the decade from 2002 to 2012 saw the “largest ever growth in energy consumption in volume terms,” but anticipates that this rate will never be exceeded in the decades to come. And they anticipate that as Chinese growth fades in the decades, so the growth of the Indian and adjacent economies will almost match that of China by the end of the period. As the nations of the world complete their industrialization, so the growth in the demand for fuel will see a greater emphasis on transportation demands.

Interestingly the decline in the demand for coal that BO projects is linked to the completion of industrialization in China, and this assumption is, of course, predicated on oil and natural gas remaining available to meet the demand at a reasonable cost.

Figure 6. Anticipated primary sources for generation of electric power.

The projections for changes in liquid fuel supply are also relatively simply presented. First one can see the projected changes in demand, with the OECD countries declining, as demand increase seems to focus in the Eastern nations.

Figure 7. Anticipated changes in global demand for liquid fuels

It is where this growth in supply is to come from that is of the greatest concern, and BP suggest the following:

Figure 8. The anticipated sources for growth in liquid fuel supply through 2035.

BP note the largest sources of these gains as being:

The largest increments of non-OPEC supply will come from the US (3.6 Mb/d), Canada (3.4 Mb/d), and Brazil (2.4 Mb/d), which offset declines in mature provinces such as the North Sea. OPEC supply growth will come primarily from NGLs (3.1 Mb/d) and crude oil in Iraq (2.6 Mb/d).One of the more interesting plots in the report shows how, over last year, the changes in US production more than compensated for the declines in production from the MENA countries.

Figure 9. The ability of increased US production to balance declines in production from the nations in turmoil in MENA.

BP anticipates that continued US increases in production will more than balance the anticipated increases in global demand, so that the continued disruptions will not significantly affect global supply even though, as they have historically, they extend for more than ten years. The US gains are anticipated to continue to such an extent that OPEC will be required to rein in their supplies in order to sustain global prices.

Figure 10. Changes in the demand for OPEC oil and the result on their production reserve capacity.

One anticipates, given that KSA has said that they will not increase overall supply much above current levels, that the increases in production that BP anticipate will likely come from Iraq, and Iran if the sanctions are lifted. Given the current situation in those parts the latter seems increasingly more likely than the former. Further BP note that the increasing populations in these countries and their consequent increases in demand for energy is likely to constrain the levels at which these countries can continue to export.

In conclusion, and to justify the heading at the top of this piece, BP anticipate a continued growth in US oil production such that, by 2035 imports are virtually eliminated, being more than offset by the gains in the export of natural gas products. BP anticipates that the latter will increase by 2025 to around 12 bcf/d and continue at about that level.

Figure 11. BP projections for changes in the US oil supply sources for the period to 2035.