It is difficult to see any positive interpretation of the changes and conflicts that are increasingly filling the headlines of the press. Fluctuating optimism over the return to credible export production from Libya, to take but one example, is no sooner reported when the news comes of increased fighting in Tripoli, including the international airport. At the same time violence is spreading towards Egypt. Without a strong central government it is likely that the conflicts in that country will continue into the foreseeable future, with continued negative impacts on the export of oil from the country.

Transient attempts to maintain a cease-fire and stabilize South Sudan have apparently failed again. The fighting has shut down local oil production, while overall production from South Sudan has been cut to 165 kbd.

Capital continues to leave Russia (h/t Nick) and that flight is only likely to accelerate as the tensions over the shooting down of the Malaysia Airlines plane continue to grow. Given that investment continues to be required to sustain Russian oil production against the current transition into decline, and that such cash is not being spent only magnifies the concern that Russian export decline will be faster and sooner than the world anticipates. (And given the critical value of Russian oil and gas exports to their economy – it provides about half the budget revenue - President Putin desperately needs a scapegoat to blame as the economic gains of the past, and future growth targets of over 5% become unrealistic dreams for that future).

With the emphasis on the daily events in all these countries (not forgetting Iraq) it is more difficult to discern the overall medium term impact that this is likely to have on oil availability, and consequently on oil and gas prices. Europe cannot function at current economic levels without the 30% of its energy that it gets from Russian natural gas, which has to be a big consideration as they discuss whether to impose more sanctions on Russia. While a recent Total study shows that, with Gazprom co-operation, Europe could cope if flows through Ukraine were stopped, without that co-operation the EU would not be able to adequately replace the lost fuel. And the conflict in Ukraine is unlikely to be resolved fairly soon, so the degree of co-operation that Western Europe can expect from Gazprom next winter is likely to lead to some fairly tense negotiations over the next few months.

One of the frustrations with watching TV pundits muse on this is that there seems to be an assumption that wells, pipelines and other necessary infrastructure will magically appear to provide immediate solutions should things start to get worse. One such today commented that President Putin is now in total control, since should the west decide not to take all of the Russian oil and natural gas that they currently consume, that he could immediately increase sales to China to replace the lost income.

That neglects the time that it is going to take to get the wells drilled in Siberia, the pipeline connections made and the receiving network in place to meet the current amount that has been sold. Even with the current agreement to increase Russian exports to China it is going to take some four years for the new gas to flow, and it took years for this agreement to be signed.

By the same token Europe can’t turn around and expect the US to be able to replace any significant amount of Russian natural gas for about a similar period of time. Facilities cannot be created overnight, and permitting and construction take finite amounts of time.

I would expect that, if anything, the price that is charged for Russian oil and gas is going to go up for the Europeans, even as the oil supply starts to decline. As Euan Mearns has noted all the significant producers of natural gas in Western Europe are seeing declines in production and while the fall last year was not that significant, overall the continued cumulative decline will make the need for Russian gas that more critical, given that the pipelines are in place to deliver it.

Unfortunately as oil and natural gas supplies continue to tighten, the natural consequence is going to be an increase in price. And this will, in turn, affect the economic growth of the different countries around the world. The current price has slowed economic growth, but as it continues to ratchet up then the impact on global growth will become rapidly obvious, although differentiated by country depending on how dependent they are on fuel imports.

Complacency within the United States, given the assumptions of indigenous supply availabilities, is likely to be shaken as internal oil supplies stop there unsustainable growth rates, while the current low prices for natural gas will disappear as the available funds for future wells reduce on the increasing evidence that most of these wells are unprofitable at current gas prices.

It is difficult – well, to be honest, impossible - for most of us to be able to see how almost any of the growing conflicts around the world can be resolved in any short-term period. The consequent impact on oil production in the countries of the Middle East and North Africa (MENA) is going to lead to a tightening of the surplus between available supply and demand, particularly at current levels. And, unfortunately, when economic circumstances grow colder political rhetoric gets hotter, and there is less chance for negotiation and diplomacy to resolve the situation.

The main surprise, at the moment, is how rapidly the situation is deteriorating in so many of the countries that supply oil and gas to the world. Sadly the headlines will only cover one or two of these at a time. As a result the overall trends are missed as headlines instead focus on the very small changes driven more by sentiment and political perspective than by the realities of the medium, and even short-term oil and gas supply situation.

Showing posts with label Chinese energy demand. Show all posts

Showing posts with label Chinese energy demand. Show all posts

Sunday, July 20, 2014

Tuesday, February 11, 2014

Tech Talk - The BP Energy Outlook 2035

BP begins its new forecast for the energy future with the statement:

Figure 1. The reducing dependence on Energy growth as a control on GDP. (All figures are from the new BP Energy Outlook for 2035)

Each year there are significant projections for the future of energy over the next few decades. Recent posts have reviewed this year’s projections from the IEA and ExxonMobil. These projections, were also reviewed last year and those reviews included the previous BP projection although that only projected forward to 2030 – the current review has added five years to this.

The relative contributions of the different fuel sources to the overall mix have not changed appreciably in the past year. Oil is anticipated to continue to shrink in percentage contribution, and coal will also decline in relative contribution after around 2020. Natural gas and renewables are anticipated to make up the supply needed.

Figure 2. Relative contributions of the different fuel sources to overall global energy supply to 2035.

BP have made it a little easier to see how this breaks down by plotting the ten-year increments in fuel contribution as well as the overall totals.

Figure 3. Changes in projected fuel supplies over the period to 2035.

Changing the plot to show the ten-year incremental changes illustrates how coal, now surging as an international fuel source, is anticipated to decline beyond 2020.

Figure 4. Projected ten-year incremental changes in fuel supply through 2035.

Note that in overall total BP is projecting that global consumption will rise by 41% over today’s numbers, most of which increase will come from the rapidly-developing countries of the world.

Figure 5. Regional increments of energy consumption growth over the decades to 2035.

The reliance on the improvements in energy efficiency to stall further growth in energy demand from the OECD countries is evident in this picture.

BP notes that the decade from 2002 to 2012 saw the “largest ever growth in energy consumption in volume terms,” but anticipates that this rate will never be exceeded in the decades to come. And they anticipate that as Chinese growth fades in the decades, so the growth of the Indian and adjacent economies will almost match that of China by the end of the period. As the nations of the world complete their industrialization, so the growth in the demand for fuel will see a greater emphasis on transportation demands.

Interestingly the decline in the demand for coal that BO projects is linked to the completion of industrialization in China, and this assumption is, of course, predicated on oil and natural gas remaining available to meet the demand at a reasonable cost.

Figure 6. Anticipated primary sources for generation of electric power.

The projections for changes in liquid fuel supply are also relatively simply presented. First one can see the projected changes in demand, with the OECD countries declining, as demand increase seems to focus in the Eastern nations.

Figure 7. Anticipated changes in global demand for liquid fuels

It is where this growth in supply is to come from that is of the greatest concern, and BP suggest the following:

Figure 8. The anticipated sources for growth in liquid fuel supply through 2035.

BP note the largest sources of these gains as being:

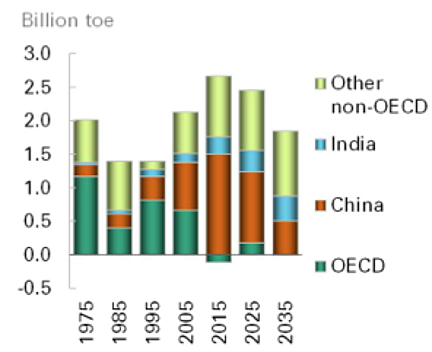

Figure 9. The ability of increased US production to balance declines in production from the nations in turmoil in MENA.

BP anticipates that continued US increases in production will more than balance the anticipated increases in global demand, so that the continued disruptions will not significantly affect global supply even though, as they have historically, they extend for more than ten years. The US gains are anticipated to continue to such an extent that OPEC will be required to rein in their supplies in order to sustain global prices.

Figure 10. Changes in the demand for OPEC oil and the result on their production reserve capacity.

One anticipates, given that KSA has said that they will not increase overall supply much above current levels, that the increases in production that BP anticipate will likely come from Iraq, and Iran if the sanctions are lifted. Given the current situation in those parts the latter seems increasingly more likely than the former. Further BP note that the increasing populations in these countries and their consequent increases in demand for energy is likely to constrain the levels at which these countries can continue to export.

In conclusion, and to justify the heading at the top of this piece, BP anticipate a continued growth in US oil production such that, by 2035 imports are virtually eliminated, being more than offset by the gains in the export of natural gas products. BP anticipates that the latter will increase by 2025 to around 12 bcf/d and continue at about that level.

Figure 11. BP projections for changes in the US oil supply sources for the period to 2035.

We project that by 2035 the US will be energy self-sufficient while maintaining its position as the world’s top liquids and natural gas producer.This illustrates the optimism which BP are projecting in their image of future production. But it carries with it a lot of inherent assumptions, some of which are relatively easy to identify in the summary graphic presentation that accompanied the initial presentation of the new report. Perhaps the most illustrative of their optimism is this plot, which shows the increasingly decoupled changes in energy supply relative to projected increases in GDP.

Figure 1. The reducing dependence on Energy growth as a control on GDP. (All figures are from the new BP Energy Outlook for 2035)

Each year there are significant projections for the future of energy over the next few decades. Recent posts have reviewed this year’s projections from the IEA and ExxonMobil. These projections, were also reviewed last year and those reviews included the previous BP projection although that only projected forward to 2030 – the current review has added five years to this.

The relative contributions of the different fuel sources to the overall mix have not changed appreciably in the past year. Oil is anticipated to continue to shrink in percentage contribution, and coal will also decline in relative contribution after around 2020. Natural gas and renewables are anticipated to make up the supply needed.

Figure 2. Relative contributions of the different fuel sources to overall global energy supply to 2035.

BP have made it a little easier to see how this breaks down by plotting the ten-year increments in fuel contribution as well as the overall totals.

Figure 3. Changes in projected fuel supplies over the period to 2035.

Changing the plot to show the ten-year incremental changes illustrates how coal, now surging as an international fuel source, is anticipated to decline beyond 2020.

Figure 4. Projected ten-year incremental changes in fuel supply through 2035.

Note that in overall total BP is projecting that global consumption will rise by 41% over today’s numbers, most of which increase will come from the rapidly-developing countries of the world.

Figure 5. Regional increments of energy consumption growth over the decades to 2035.

The reliance on the improvements in energy efficiency to stall further growth in energy demand from the OECD countries is evident in this picture.

BP notes that the decade from 2002 to 2012 saw the “largest ever growth in energy consumption in volume terms,” but anticipates that this rate will never be exceeded in the decades to come. And they anticipate that as Chinese growth fades in the decades, so the growth of the Indian and adjacent economies will almost match that of China by the end of the period. As the nations of the world complete their industrialization, so the growth in the demand for fuel will see a greater emphasis on transportation demands.

Interestingly the decline in the demand for coal that BO projects is linked to the completion of industrialization in China, and this assumption is, of course, predicated on oil and natural gas remaining available to meet the demand at a reasonable cost.

Figure 6. Anticipated primary sources for generation of electric power.

The projections for changes in liquid fuel supply are also relatively simply presented. First one can see the projected changes in demand, with the OECD countries declining, as demand increase seems to focus in the Eastern nations.

Figure 7. Anticipated changes in global demand for liquid fuels

It is where this growth in supply is to come from that is of the greatest concern, and BP suggest the following:

Figure 8. The anticipated sources for growth in liquid fuel supply through 2035.

BP note the largest sources of these gains as being:

The largest increments of non-OPEC supply will come from the US (3.6 Mb/d), Canada (3.4 Mb/d), and Brazil (2.4 Mb/d), which offset declines in mature provinces such as the North Sea. OPEC supply growth will come primarily from NGLs (3.1 Mb/d) and crude oil in Iraq (2.6 Mb/d).One of the more interesting plots in the report shows how, over last year, the changes in US production more than compensated for the declines in production from the MENA countries.

Figure 9. The ability of increased US production to balance declines in production from the nations in turmoil in MENA.

BP anticipates that continued US increases in production will more than balance the anticipated increases in global demand, so that the continued disruptions will not significantly affect global supply even though, as they have historically, they extend for more than ten years. The US gains are anticipated to continue to such an extent that OPEC will be required to rein in their supplies in order to sustain global prices.

Figure 10. Changes in the demand for OPEC oil and the result on their production reserve capacity.

One anticipates, given that KSA has said that they will not increase overall supply much above current levels, that the increases in production that BP anticipate will likely come from Iraq, and Iran if the sanctions are lifted. Given the current situation in those parts the latter seems increasingly more likely than the former. Further BP note that the increasing populations in these countries and their consequent increases in demand for energy is likely to constrain the levels at which these countries can continue to export.

In conclusion, and to justify the heading at the top of this piece, BP anticipate a continued growth in US oil production such that, by 2035 imports are virtually eliminated, being more than offset by the gains in the export of natural gas products. BP anticipates that the latter will increase by 2025 to around 12 bcf/d and continue at about that level.

Figure 11. BP projections for changes in the US oil supply sources for the period to 2035.

Read more!

Tuesday, August 14, 2012

OGPSS - Considerations of Chinese demand growth

Three years ago I took my third trip to China, flying this time to Qinghai Province and then taking the train back down from Xining City through Xian to Shanghai. One of the more striking parts of the trip was the first day of the train travel, where the tracks cut down from the Tibetan Plateau to the plains of the East. The valleys are narrow, so that it is often difficult for the train tracks and road to find an easy route, and this led to many tunnels, and, in places, one or the other running on piers up the valley.

Figure 1. Railway causeway set across a valley carrying a second line (photo taken from the first, about to go into a tunnel) the river crosses under the line and runs along the left hillside.

Figure 1. Railway causeway set across a valley carrying a second line (photo taken from the first, about to go into a tunnel) the river crosses under the line and runs along the left hillside.

The countryside was redolent with new construction of highways, and the necessary tunnels to bring additional communications into a hinterland that had, in the past, few good roads or methods of reaching into the more remote communities.

Figure 2. Further down the valley it is much narrower and the road and rails run in tunnels (on each side of the river). The current narrow road is being widened but whenever there was a hold-up, the line of trucks waiting grew by miles. (Very few cars).

A historian once commented on the major impact to the American economy and social infrastructure created with the development of the road network and the addition of the Interstate system. When I first went to China in 1987 poverty was rampant, the main method of transportation was by bicycle though I travelled by train and minibus. By the time of the second visit in 2002 the economy was undergoing rapid changes. Their interstate network was being developed, although I remember noting that the train passed many miles of freeway with very little traffic. They are now seeing this gain, but it is a work still in progress, and it, in turn is driving the growth in their oil demand.

Figure 3. Changes in Chinese oil consumption and imports over the past decades (Energy Export Databrowser )

It is important to recognize that there are many parts of the country where these interconnections and improvements to the infrastructure are still going on, and as those changes occur so the increasing use of power-driven vehicles continues to rise, and with it the need for increased supply. The risk of exacerbating popular unrest if that change were to stop is just one reason why it is bound to continue, and with it China’s continued need for additional supplies of all forms of fossil fuels, as well as the rest of those supplies that we all need that come from the earth. And that includes water, a vital resource, but one whose limit restricts some of the options that the Chinese government can adopt.

In the July Monthly Oil Market Report, OPEC note that automobile sales in China were up for May by 22% y-o-y , though this is not expected to change the rate of growth in overall oil demand for the country. In total they expect, as they noted in August, China’s economic growth forecast remains at 8.1%, with an 8% projection for 2013.

Figure 4. Changes in apparent oil demand for China (OPEC August MOMR)

Within that overall demand the relative proportions of the mix change, over time., though it must be remembered, in this regard that China is still building a Strategic Petroleum Reserve of its own, and up to 1 mbd can be fed into this when judged appropriate.

Figure 5. Change in apparent oil consumption in China (OPEC August MOMR)

Figure 5. Change in apparent oil consumption in China (OPEC August MOMR)

The problems of traffic congestion, exemplified by the 11-day Beijing traffic blockage in 2010 is leading to some restrictions within the cities. Four cities (Beijing, Shanghai, Guiyang and Guangzhou are now said to restrict car sales (OPEC August MOMR) and electrical vehicles and taxis are being introduced, with a target of half-a-million vehicles by 2015. This is now seen as an area of growth, especially in battery development, and a target of 5 million cars has been set for 2020. And while this might seem to be a market opportunity for the Volt, domestic tax protection has made it a difficult sale to the present.

And a recent report by the Economist indicates that sales of these vehicles have not taken off as hoped, with only 8,000 being sold, largely to government agencies. As in the United States there is an element of “chicken and egg” to the story, in that without a network of charging stations there is a certain amount of caution in committing a higher than normal investment without the assurance of benefit in the very near future. The suggestion is that China may backtrack to a greater emphasis on hybrids before returning to push for the purely electrical car.

This is not to say that there is not a recognition of the need for alternate sources of energy. But in China the general populace has a much better understanding of the limited nature of energy supplies, a lesson that the rest of us will likely have to learn another way. Thus one finds a much wider use of solar power, including for the more mundane use in making tea. It was instructive to see, as we drove down a street in one of the tourist resort towns near a lake, that each house along the street had a large kettle sitting outside, on a solar collecting dish.

Figure 5. Solar heating of a kettle (30 min to boiling)

Many had solar water heaters on the roof also, and while somewhat more unsightly than many systems (mine for example is black plastic solar pipes that blend into the roof) they take up less space and serve their purpose.

Figure 6. Solar water heater (cost around $1,000 installed)

I came away convinced that China is nowhere near the point where it can meet the growing demands that a developing society will have for energy, and that their government will be driven to find creative ways of meeting that increasing demand.

Figure 1. Railway causeway set across a valley carrying a second line (photo taken from the first, about to go into a tunnel) the river crosses under the line and runs along the left hillside.

Figure 1. Railway causeway set across a valley carrying a second line (photo taken from the first, about to go into a tunnel) the river crosses under the line and runs along the left hillside. The countryside was redolent with new construction of highways, and the necessary tunnels to bring additional communications into a hinterland that had, in the past, few good roads or methods of reaching into the more remote communities.

Figure 2. Further down the valley it is much narrower and the road and rails run in tunnels (on each side of the river). The current narrow road is being widened but whenever there was a hold-up, the line of trucks waiting grew by miles. (Very few cars).

A historian once commented on the major impact to the American economy and social infrastructure created with the development of the road network and the addition of the Interstate system. When I first went to China in 1987 poverty was rampant, the main method of transportation was by bicycle though I travelled by train and minibus. By the time of the second visit in 2002 the economy was undergoing rapid changes. Their interstate network was being developed, although I remember noting that the train passed many miles of freeway with very little traffic. They are now seeing this gain, but it is a work still in progress, and it, in turn is driving the growth in their oil demand.

Figure 3. Changes in Chinese oil consumption and imports over the past decades (Energy Export Databrowser )

It is important to recognize that there are many parts of the country where these interconnections and improvements to the infrastructure are still going on, and as those changes occur so the increasing use of power-driven vehicles continues to rise, and with it the need for increased supply. The risk of exacerbating popular unrest if that change were to stop is just one reason why it is bound to continue, and with it China’s continued need for additional supplies of all forms of fossil fuels, as well as the rest of those supplies that we all need that come from the earth. And that includes water, a vital resource, but one whose limit restricts some of the options that the Chinese government can adopt.

In the July Monthly Oil Market Report, OPEC note that automobile sales in China were up for May by 22% y-o-y , though this is not expected to change the rate of growth in overall oil demand for the country. In total they expect, as they noted in August, China’s economic growth forecast remains at 8.1%, with an 8% projection for 2013.

Figure 4. Changes in apparent oil demand for China (OPEC August MOMR)

Within that overall demand the relative proportions of the mix change, over time., though it must be remembered, in this regard that China is still building a Strategic Petroleum Reserve of its own, and up to 1 mbd can be fed into this when judged appropriate.

The problems of traffic congestion, exemplified by the 11-day Beijing traffic blockage in 2010 is leading to some restrictions within the cities. Four cities (Beijing, Shanghai, Guiyang and Guangzhou are now said to restrict car sales (OPEC August MOMR) and electrical vehicles and taxis are being introduced, with a target of half-a-million vehicles by 2015. This is now seen as an area of growth, especially in battery development, and a target of 5 million cars has been set for 2020. And while this might seem to be a market opportunity for the Volt, domestic tax protection has made it a difficult sale to the present.

And a recent report by the Economist indicates that sales of these vehicles have not taken off as hoped, with only 8,000 being sold, largely to government agencies. As in the United States there is an element of “chicken and egg” to the story, in that without a network of charging stations there is a certain amount of caution in committing a higher than normal investment without the assurance of benefit in the very near future. The suggestion is that China may backtrack to a greater emphasis on hybrids before returning to push for the purely electrical car.

This is not to say that there is not a recognition of the need for alternate sources of energy. But in China the general populace has a much better understanding of the limited nature of energy supplies, a lesson that the rest of us will likely have to learn another way. Thus one finds a much wider use of solar power, including for the more mundane use in making tea. It was instructive to see, as we drove down a street in one of the tourist resort towns near a lake, that each house along the street had a large kettle sitting outside, on a solar collecting dish.

Figure 5. Solar heating of a kettle (30 min to boiling)

Many had solar water heaters on the roof also, and while somewhat more unsightly than many systems (mine for example is black plastic solar pipes that blend into the roof) they take up less space and serve their purpose.

Figure 6. Solar water heater (cost around $1,000 installed)

I came away convinced that China is nowhere near the point where it can meet the growing demands that a developing society will have for energy, and that their government will be driven to find creative ways of meeting that increasing demand.

Read more!

Subscribe to:

Posts (Atom)