Since I started writing about peak oil back in 2005, the possible maximum sustainable production achievable from the Kingdom has been one of the recurring issues at The Oil Drum, and there have been a number of very perceptive analyses carried out by folk such as Euan Mearns, Stuart Staniford, and JoulesBurn that I do not intend to try and surpass. I will, however, try and summarize some of their conclusions as I work through a few posts that look at the overall production from the various fields that are found both on and offshore Saudi Arabia.

As an initial point, not all the oil that comes from the country is of the same quality, and this is often one of the initial factors that folk do not appreciate when they look, for example, at the two numbers I gave above, that which the KSA is producing, relative to that which it might be able to achieve. The problem arises with the heavier crudes that make up a part of the surplus, and for which there is not a great market out there, as yet. So let me begin the review with, this week, just simply looking at an overall view of the country, the oilfields that comprise regions of major production and what sort of oil that they are producing.

Back in 2005, production from the different oil fields added up to 9.07 mbd, and at the time I had figures suggesting that the total broke down as follows:

Abqaiq 400 kbd;JoulesBurn has since pointed to me that my initial attributions were incorrect and that, in a paper given in 2006, Mendez et al had reported that the target for Hout was only 50 kbd, while that for Khafji was 300 kbd. I will explore those issues more in later posts on this region. But a hat tip to JB for catching my error.

Abu Sa'fah 200 kbd;

Berri 300 kbd;

Ghawar 4,500 kbd;

Hawtah 200 kbd;

Hout 300 kbd;

Khurais 300 kbd;

Marjan 270 kbd;

Qatif 800 kbd;

Safaniya 700 kbd;

Shaybah 600 kbd; and

Zuluf 500 kbd.

This adds up methinks to 9.07 mbd.

The major fields in Saudi Arabia (EIA)

The major fields in Saudi Arabia (EIA)Not all these fields have oil of equivalent quality, and this is a point that often fails to be understood when there is a global shortage and the KSA offers more crude to the market. If that crude is sufficiently sour (i.e. too much sulfur) and heavy (low API gravity) then it cannot be refined by some of the refineries that may be hurting the most. Thus the oil might not find a market, even though there is a shortage. What the KSA tries to do is to swap deliveries, but that does not always work as it might.

Different grades of oil supplied by Saudi Arabia.

Different grades of oil supplied by Saudi Arabia. (For those who have forgotten the API gravity classification in degrees, I explained it in an earlier post. Suffice it to say that the higher the number, as a general rule, the lighter the crude and the better the market. As the share produced from the historic fields changes, so the KSA has offered the heavier crudes to the market, but, as I noted, even with the increase in global demand, those crudes have been less successful in finding a permanent market.)

Way back when the world was more innocent, there were four major fields that produced most of the oil from KSA:

Ghawar (the King), which started producing in 1951. Peak production was at 6.6 mbd. Current production is under 5 mbd. Water inflow percentages are increasing, and overall output is decreasing. It is divided into various regions, Ain Dar oil has an API gravity of 34, and 1.66% sulfur. Shedgum is at an API gravity of 34 and sulfur content of 1.75%. Uthmaniyah has an API of 33, and 1.91% sulfur. Hawiyah is at an API gravity of 32,and 2.13% sulfur, while Haradh oil has an API gravity of 32 and 2.15% sulfur. The levels of sulfur define how “sour” the crude is, and this must be recognized by the refineries, such as the Fujian Refinery in Quanzhou, China which is designed to refine 240 kbd of sour light Arabian crude. The oil from Ghawar flows to the Abqaiq processing plant, this can handle up to 7 mbd of light and extra-light crude., and cleans the crude before sending it on to refineries at Ras Tanura, Jubail, Yanbu and Bapco.

Abqaiq (The Queen) saw peak production in 1973 at 1 mbd, has now fallen to a level of around 200 kbd. It is a field that is “rested” from time to time in order to sustain an even displacement as the water flood progresses. The oil is at API 36.

Safaniya (2nd Queen) started producing at 50 kbd from 8 wells in 1957, peak production was at 1 mbd, and is now down to about 770,000bd. The field lies offshore, and is a producer of some of the heavier crudes, with an API gravity of 26, and a sulfur content of up to 2.96%. It has a current production capacity of 1.2 mbd, but because of the heavier nature of the oil has more trouble in finding a world market, and thus often much of this production is withheld. (In 2008, for example some 700 kbd was being withheld from the market.) The field is currently being further developed with a larger pipeline being installed to allow a higher flow rate from the field onshore. It is also intended that the gas that is now flared will be captured. The upgrade will also involve the installation of submersible pumps and an upgrade to the distribution network, and is scheduled for completion in late 2013, when the capacity will rise to 1.5 mbd.

Berri (the Great Lord) saw peak production at 788,000 bd in 1977 and more recently that fell to around 300,000 bd. This was the fourth of the original set of fields in Saudi Arabia that were responsible for 93% of Saudi production back in 1978. It is slowly watering out and has been occasionally left resting except when additional production is required. The oil has an API gravity of 38, with about 1% sulfur. The field has been reworked so that it now has a capacity of 1.15 mbd though some 300 kbd of this is considered part of the reserve production in case of need, rather than normal production.

Looking back seven years, the plans that the kingdom had, back then, for sustained and increasing production (they recognized that existing wells would decline and thus planned for their replacement) were clearly stated by Abd Allah Al-Saif :

major projects that Saudi Aramco is undertaking to ensure meeting future demand:

The Abu Sa'fah and Qatif projects came on stream in 2004 adding 650,000 bpd.

300,000 bpd of Arabian Light will come on stream in the Haradh field in mid-2006.

500,000 bpd of Arabian Light will be added to capacity through the Khursaniyah development, planned for 2007.

2008 is the target date of approved expansion plans that would add 300,000 bpd of lighter crude at Shaybah and central Arabian fields.

A Khurais increment of 1.2 million bpd of Arabian Light will be commissioned in 2009.

"This is a very aggressive program that will require the mobilization of immense resources, such as rigs, material and manpower, but which we are confident to successfully execute, as we have done for the past 70 years," he said.

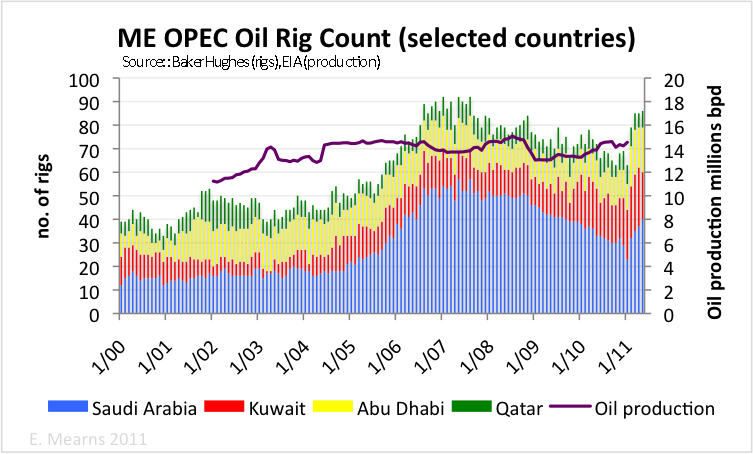

Concerns at the time, over the ability of the kingdom to meet these plans focused not only on the quality of the mix, but were more immediately initially aimed on the number of drilling rigs that the KSA had available to drill the required number of wells. Back in 2005 the country did not have a whole lot of rigs at their disposal. This has since been highlighted by Euan Mearns:

Rig Count for the Middle East (Euan Mearns 2011)

Rig Count for the Middle East (Euan Mearns 2011) Bear in mind that when we started posting we were just coming to the end of the relatively flat section of the Saudi plot, and were, at the time, unable to see how they could continue operations with only 20 odd rigs. Well, with hindsight they could not, and as the plot suggests they rapidly acquired all the spare rigs available at the time and this allowed the increase in the number of wells that afforded the new levels of overall production. Sam Foucher has also posted on the rig count, and his plot agrees more with my memory of the dramatic transition in rigs that the KSA employed back in the 2006-7 timeframe to move them from the placid conditions pre-2005 to the sudden realization that BAU would no longer work.

Various Saudi plots from Sam, though the critical one is the rig count change (Sam Foucher)

Various Saudi plots from Sam, though the critical one is the rig count change (Sam Foucher)The point of the illustration is to indicate that circumstances do change operating conditions, and that folk do respond when they have to. Up, that is, to the limits that they are able to achieve. Some of those limits are imposed by the fact that you cannot suck beer from a conventional pint glass forever, as I discovered when in college, and it is in regard to those issues as well as some more of the above that the discussion will swing toward as the next few weeks unfold.

There have been many other posts on the subject on the Oil Drum over the years, (if one includes Drumbeat there are more than 2,000) here are but a very few

JoulesBurn- Abqaiq

Intro to Satellite sleuthing

Khurais me a river

Happenings in Harmaliyah

Ghawar Numerology

Stuart Staniford

Satellite o’er the desert

Euan Mearns

Saudi Production laid bare

I will add to this list as I move on and start to address some of the concerns that have been raised.

Normandy Inn

Carmel-by-the-Sea

{kind=link}

Just saw your reference to the Persian Gulf as arabian gulf.

ReplyDeleteIt is, and will always remain, the Persian Gulf, you pieces of shit motherfcukers.

We only say once, remove that fcuking bullshit name or else!!!!

The Saudi Arabia is a supreme organization

ReplyDeleteal saif motors feedback