One of the changes in reality that is likely to have significant impact in the near-term is the flow in the Alyeska pipeline. Long-time concerns over the decline in flow and the effect that heat loss has on the contents is leading to new work to change the pipe dynamics and possibly to remove the water before it is pumped, lowering the temperatures at which the line currently has to be maintained.

Figure 1. Historic and Projected flows through the Alaskan pipeline (Alyseka)

The precipitation of ice and water from the oil, within the pipeline will otherwise reach a point that flow will stop – potentially at around 300 kbd, at a date not too far into the future.

In their annual World Energy Outlook, the IEA continue to see, overall, a gain in US oil production through 2025, largely coming through the light tight oil of the sort being produced from North Dakota and West Texas.

Figure 2. IEA projections for global oil production growth in the years to 2035. (IEA)

However in the following years , out to 2035, that supply also declines so that by 2035 the US will likely be in the same sort of supply situation, relying heavily on imports, that it is today.

The IEA make the point that the only longer term places that can be relied on are Brazil, with the off-shore fields, and the Middle East. Looking first at Brazil, which continues to have some problems in bringing their fields on-line on-schedule, the IEA anticipates that the major production growth is likely to be in the next ten years, but will continue beyond that point.

Figure 3. Brazilian oil production through 2035. (IEA)

Because the IEA foresee that Brazil will continue to supply the largest portion of its energy from hydropower this means that the largest volume of the fuel can be exported, where it meets the continually growing demand from the rest of the world.

Figure 4. Anticipates sources of power for electricity generation in 2035 (IEA)

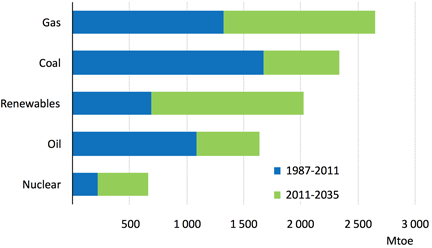

At the same time the IEA anticipate that primary energy demand will still focus heavily on fossil fuel sources through 2035, with renewable energy only slowly nibbling away at the totals so that, by 2035 fossil fuel will have dropped from contributing the current 82% down to 75% of the larger total.

Figure 5. Anticipated changes in the sources of primary global energy through 2035. (IEA)

Although, by that time the IEA foresee a change not only in the places where demand is highest, but also in the relative rankings. The major finding in this regard that they draw attention to is the anticipated greater growth rates in India than in China, as time passes.

Figure 6. Changed picture of global energy demand in the year 2035 (IEA)

Other than projecting the growth in demand there is the need to anticipate where the supply will come from, and in this regard the IEA projects that the largest growth will come from natural gas (Figure 5), although crude oil is still anticipated to grow, with refinery capacity increasing to about 104 mbd.

It is interesting that the IEA projections for oil production growth hang most heavily on increased production from the Middle East. It requires very little glance into their crystal ball to assume that this is likely based on the increased production from Iraq, an assumption that was, last year, a largely common assumption to all future projections. Unfortunately for those earlier projections in the interim the initial Iraqi targets have been cut back, with current targets being reduced below the “best case” scenario that the IEA had projected in their review of the country.

Taken with the possibility of a significant and sudden decline in production from Alaska, and the likelihood that the rate of drilling in the Bakken will decline, as prospects become more uneconomic suggests that it will be difficult to sustain the levels of crude output that the IEA are anticipating can be made available to meet their projected needs.

By the same token the growth in the global demand for natural gas is predicated on the reserves uncovered in the United States being exported, as needed, to the rest of the world. It is, however, also predicated on the price of natural gas remaining relatively stable in terms of current costs.

Figure 7. Anticipated components of the costs of US LNG when shipped to either Asia or Europe (IEA)

The underlying flaw in that assumption is that the costs of purchasing the natural gas in the United States are now starting to rise to a more realistic level relative to the costs of production from tight shales. This week's OGJ, for example has noted the EIA Short Term Energy and Winter Fuels outlook that notes that prices are expected to rise 13% this winter over last (on constant demand) to $3.62 per kcf. Given that the EIA is expecting the price to inch upwards towards $5.00 per kcf over the next year this makes the IEA report appear a little over-optimistic on costs and hence market share.

Figure 8. Natural Gas Prices in the United States (EIA)

This is likely to be particularly true as some of the older gas fields, such as the Haynesville, appear to be in decline even at prices in the $4 - $5 per kcf range.

Figure 9. Natural Gas Production from the Haynesville Shale (OGJ )

Increasing the price of natural gas will reduce its competitive advantage over coal and in consequence I would anticipate that power generating companies will continue to build boilers that can handle both coal and natural gas, and that the longer-term continued switch to natural gas will become more of an economic choice dependent on how much LNG finally comes onto the market from the United States and at what price. I am not convinced that this will be quite the bargain and cornucopia that it is anticipated to become. In other words I still find the IEA view of the future to be a somewhat optimistic one, given the realities that are now unfolding before us.

prodigy oil and gas are the best place to invest for power industry

ReplyDeleteWe Can supply Aviation Kerosene,Jet fuel (JP 54-A1,5), Diesel (Gas Oil) and Fuel Oil D2, D6,ETC in FOB/Rotterdam only, serious buyer should contact or if you have serious buyers my seller is ready to close this deal fast contact us below:now base email us (neftegazagent@yandex.ru)

ReplyDeletePRODUCT AVAILABLE IN ROTTERDAM/ CI DIP AND PAY IN SELLER EX-SHORE TANK.

Russia D2 50,000-150,000 Metric Tons FOB Rotterdam Port.

JP54 5000,000 Barrels per Month FOB Rotterdam.

JA1 Jet Fuel 10,000,000 Barrels FOB Rotterdam.

D6 Virgin Fuel Oil 800,000,000 Gallon FOB Rotterdam.

E-mail: neftegazagent@yandex.ru

E: neftegazagent@mail.ru

E: neftegazagent@yahoo.com

Best Regards

(Mr.) Vladislav Yakov

Skype: neftegazagent

Thank You