It is perhaps an odd time to be writing about oil shortages. The price of gas in our town has just moved above $2 a gallon up significantly from the $1.64 it was at its recent lowest point, but still very reasonable. Debate still rages as to whether the global price of a barrel of oil has found a bottom, although there are signs that the price is beginning to increase, in part due to other issues than overall availability of crude. So why be concerned?

There are several issues, and perhaps the first is that of industrial inertia. Despite the daily fluctuations in oil price, many of the events that occur between the time that oil is found in a layer of rock underground and the time that some of it is poured into your gas tank take a long time to initiate, and similarly can’t be turned off overnight. It takes, for example, roughly 47 days for a tanker to travel from Ras Tanura in Saudi Arabia to Houston.

One response to the drop in oil prices has been to reduce the number of rigs drilling for oil in the United States. Again this is not an immediate response, but rather one that grows with time. This is particularly true with the number of oil rigs that are used to gain access to the oil reservoirs. As the price for this oil falls, so rigs are idled and the potential for additional oil production also declines. This drop is particularly significant in fields that are horizontally drilled and fracked because of the very rapid decline in production with time in existing wells and the need for continued drilling to develop and produce new wells to sustain and grow production. The most recent figures show a fall of 98 rigs in the week from the 6th to the 13th of February, with the overall count now standing at 1,358. This rate of decline has held at nearly 100 rigs a week now for the past three with no indication of any immediate change in the slope of the curve. At the same time the number of well completions in the Bakken is falling, as producers hold back on the costs for producing oil that would be sold at a loss.

The impact from this will take time to appear, North Dakota has reached a production rate of 1.2 mbd in December and the DMR estimates that it will need around 140 rigs to sustain that production level this year, with the most recent rig count being 137. This number is likely to continue to fall through the first six months of the year.

The impact is not just in the immediate loss of production. Rather, once the rigs are idled it will take time, even after the markets recover, for the companies to adjust their planning and finances, and to re-activate the rigs. What this effectively does is to shift the production increment into later years, when the production base from existing wells will have declined beyond current levels. This means that the peak level of production will likely also be lower than would otherwise be the case, and the period over which this peak production is sustained will also be shorter.

The problem that this all presages is that lower levels of production against an increasing world demand will induce a faster rise in price than many now anticipate. There is a complacent feeling that oil prices won’t reach $100 a barrel for some considerable time - perhaps even years. If the current difference between available oil supply and demand is below 2 mbd, Euan Mearns has suggested that roughly half of this might be eaten up by increased demand, while the other half would disappear as production levels drop, although he doesn’t see this bringing the two volumes into rough balance until the end of 2016.

I rather think that it will happen faster than that, and that the price trough will steepen faster than currently anticipated, and likely before the end of this year. The problem (if you want to call it that) with the perceptions of the ability of global production to meet demand is that it is all tied to the production of the United States and Canada. I have noted, over the past two years, how future projections of increasing global oil demand have been met, in models, by increased production from the United States, and that this was anticipated to continue. (Increased production from Iraq, if sustained, is more likely to be needed just to balance declines in production from other countries).

Yet the US industry is going into a relatively rapid decline because of the way that it is structured that is going to be hard to stop, and much slower to reverse than anticipated. (In a way it is similar to the intermittent traffic congestion one finds on roads which result because we brake a lot faster than we then accelerate). This will not only stop the growth in production that is currently anticipated, but will go further and before the end of the year will lead to a drop in overall volumes produced. Yet demand is expected to increase. Where will the supply come from, if not the United States?

While Saudi Arabia can produce more, one gets the sense that they are quite comfortable where they are, thank you and won’t be increasing their contribution, and while Russia may bemoan the price they are getting for their oil, if the price goes up they are not going to be able to meet an increased demand, nor are there likely to be others with spare capacity that they can bring to the table. And because of the inertia in the system the United States will still be in a mode of declining production.

So I rather suspect that what we can anticipate is that prices will start to recover through the summer, and then, as the full impact of the rebalanced situation starts to become evident, will move higher at an increasing rate. Because if, in fact, we are reaching the period of a tighter balance between demand and available supply, then the market will change its perceptions quite quickly and be driven by a totally different metric.

Showing posts with label Saudi crude production. Show all posts

Showing posts with label Saudi crude production. Show all posts

Monday, February 16, 2015

Monday, October 6, 2014

Tech Talk - The Price of Power, and its consequences

The changing colors of the leaves carry the message that winter will soon be here, and so it is time to stock the yard with wood to carry us through until spring. In Missouri I just found wood, cut to the length I need, and stacked, for $110 a cord and (since it has to be cut) it will arrive next week. Only the chimney then needs a quick sweep, and we’ll be ready for another season. (We burn just under a cord of wood a month, and this keeps the electricity bill sensible).

At one time the wood was insurance, in case of an extended power outage (and we had one that lasted three days, one winter) but we enjoy the heat from the tile stove, and so it is now part of our life. And with the continued risk of a loss of power, the insurance remains comforting.

Driving back from Maine a couple of weeks ago, gas prices fell over $0.25 a gallon along the 1,300 mile trip, another benefit of living in the Mid-West. But at both ends of the drive, the impact of fuel prices continues to slow economic growth, as it does nationally. Gail Tverberg has written of the inter-relation between the economy and fuel prices, most recently on Monday. However we disagree on one point, since she anticipates a potential significant drop in oil prices, which I do not.

In the early days of The Oil Drum I remember walking through the streets of Denver to a meeting with two other contributors, and suddenly realizing that I, the more technically based of the three, was by far the most pessimistic. Increasingly I am realizing that while this pessimism has not ameliorated, the current relative abundance of oil and gas in the United States has given many folk an undeservedly complacent view of the next few years.

Ron Patterson recently pointed out that if one discounts US production, the rest of the world has seen a decline in production, with non-US production now down around 2 mbd from its all-time peak. (If one also removes Saudi Arabian and Russian production from the mix, the decline gets closer to 3 mbd). Now to assume that this is totally due to a loss in production capacity would be a mistake. Saudi Arabia continues to adjust the volume of their production to try and keep global prices relatively stable, dropping production by 400 kbd in August. In the immediate short-term that was not enough for their purpose, and they are now lowering price a little, perhaps in order to sustain their market share. The cuts were in the range of $0.20 to $1.20 a barrel). Although it could also be a way of trying to sustain global growth at a time of weakness.

Figure 1. Global Production without including the United States – as plotted by Ron Patterson. I added the trend line at the end of the top plot.

These flutterings at the margin however don’t help my concerns, because they are focused only on the short-term, and don’t consider the overall situation. If the production from the rest of the world is declining at around 700 kbd, and Saudi Arabia will only produce to a maximum of 10 mbd, and Russia appears to be in that plateau that precedes decline, even without the loss in funding that recent US Government mandates will impose, then that leaves the growth in US production as being the only source to match both the decline in global production, and the continuing demand for more oil which together total around 1.7 mbd. And US production projections, even at their most optimistic can’t do this, even for one more year.

Figure 2. Projected Growth in US production (EIA)

The mathematics are, of course, not absolute numbers but remain somewhat flexible. There could be a sudden cessation of conflict in Libya and full production might return; all conflict might end in Iraq and production development might surge at the investment opportunity; and sanctions might disappear against Iran – but somehow I don’t see any of these happening.

The argument of the Cornucopians, that one can either find a substitute for the fuel in some other resource, or that technology will suddenly become available to allow unanticipated levels of production from the existing reserves and resources is, perhaps why I – knowing a fair bit about the technology – am more of a pessimist than many others.

The analogy that I use may be a little crude – but you can’t have a baby in a month by making nine women pregnant. You can’t create new technology out of thin air by suddenly investing a few billion in a bunch of scientists pulled from lists on the Internet either. There are not that many folk who are sufficiently expert to be useful, particularly in the fields that relate to the production of fossil fuels. Many of those who do exist are, like me, coming to the end of their professional lives, so that the skill sets and knowledge bases that they have built are disappearing. Many of the doctorates that we see today are based more on computer modeling than on hands-on experimentation and engineering. And unfortunately the knowledge that we have about the nature of the rocks at depth, their behavior and how to change the way in which they yield their fluids still leaves a lot to be desired, when it comes to validating the models that are produced.

But even if such new technology were developed it would take decades to see it adopted in sufficient volume across the world that it would have a significant impact on global fuel production. It was for this reason that, back in 2005, the Hirsh Report discussed the need for a twenty-year lead-time to develop new technology that could replace our needs for fuel. The time that they suggested that we had available now is beginning to seem very optimistic, while the moves to ameliorate the problem have been judged less critical and thus no longer receive the attention and funding that the have in the past.

And so, when the crisis comes, and this is increasingly likely to come in the next two years, there will be no good answers, just tightening supplies and rising prices. This is perhaps why I am beginning to think that the next President of the United States still may well be, despite all the gaffs, Brian Schweitzer.

At one time the wood was insurance, in case of an extended power outage (and we had one that lasted three days, one winter) but we enjoy the heat from the tile stove, and so it is now part of our life. And with the continued risk of a loss of power, the insurance remains comforting.

Driving back from Maine a couple of weeks ago, gas prices fell over $0.25 a gallon along the 1,300 mile trip, another benefit of living in the Mid-West. But at both ends of the drive, the impact of fuel prices continues to slow economic growth, as it does nationally. Gail Tverberg has written of the inter-relation between the economy and fuel prices, most recently on Monday. However we disagree on one point, since she anticipates a potential significant drop in oil prices, which I do not.

In the early days of The Oil Drum I remember walking through the streets of Denver to a meeting with two other contributors, and suddenly realizing that I, the more technically based of the three, was by far the most pessimistic. Increasingly I am realizing that while this pessimism has not ameliorated, the current relative abundance of oil and gas in the United States has given many folk an undeservedly complacent view of the next few years.

Ron Patterson recently pointed out that if one discounts US production, the rest of the world has seen a decline in production, with non-US production now down around 2 mbd from its all-time peak. (If one also removes Saudi Arabian and Russian production from the mix, the decline gets closer to 3 mbd). Now to assume that this is totally due to a loss in production capacity would be a mistake. Saudi Arabia continues to adjust the volume of their production to try and keep global prices relatively stable, dropping production by 400 kbd in August. In the immediate short-term that was not enough for their purpose, and they are now lowering price a little, perhaps in order to sustain their market share. The cuts were in the range of $0.20 to $1.20 a barrel). Although it could also be a way of trying to sustain global growth at a time of weakness.

Figure 1. Global Production without including the United States – as plotted by Ron Patterson. I added the trend line at the end of the top plot.

These flutterings at the margin however don’t help my concerns, because they are focused only on the short-term, and don’t consider the overall situation. If the production from the rest of the world is declining at around 700 kbd, and Saudi Arabia will only produce to a maximum of 10 mbd, and Russia appears to be in that plateau that precedes decline, even without the loss in funding that recent US Government mandates will impose, then that leaves the growth in US production as being the only source to match both the decline in global production, and the continuing demand for more oil which together total around 1.7 mbd. And US production projections, even at their most optimistic can’t do this, even for one more year.

Figure 2. Projected Growth in US production (EIA)

The mathematics are, of course, not absolute numbers but remain somewhat flexible. There could be a sudden cessation of conflict in Libya and full production might return; all conflict might end in Iraq and production development might surge at the investment opportunity; and sanctions might disappear against Iran – but somehow I don’t see any of these happening.

The argument of the Cornucopians, that one can either find a substitute for the fuel in some other resource, or that technology will suddenly become available to allow unanticipated levels of production from the existing reserves and resources is, perhaps why I – knowing a fair bit about the technology – am more of a pessimist than many others.

The analogy that I use may be a little crude – but you can’t have a baby in a month by making nine women pregnant. You can’t create new technology out of thin air by suddenly investing a few billion in a bunch of scientists pulled from lists on the Internet either. There are not that many folk who are sufficiently expert to be useful, particularly in the fields that relate to the production of fossil fuels. Many of those who do exist are, like me, coming to the end of their professional lives, so that the skill sets and knowledge bases that they have built are disappearing. Many of the doctorates that we see today are based more on computer modeling than on hands-on experimentation and engineering. And unfortunately the knowledge that we have about the nature of the rocks at depth, their behavior and how to change the way in which they yield their fluids still leaves a lot to be desired, when it comes to validating the models that are produced.

But even if such new technology were developed it would take decades to see it adopted in sufficient volume across the world that it would have a significant impact on global fuel production. It was for this reason that, back in 2005, the Hirsh Report discussed the need for a twenty-year lead-time to develop new technology that could replace our needs for fuel. The time that they suggested that we had available now is beginning to seem very optimistic, while the moves to ameliorate the problem have been judged less critical and thus no longer receive the attention and funding that the have in the past.

And so, when the crisis comes, and this is increasingly likely to come in the next two years, there will be no good answers, just tightening supplies and rising prices. This is perhaps why I am beginning to think that the next President of the United States still may well be, despite all the gaffs, Brian Schweitzer.

Read more!

Sunday, August 10, 2014

Tech Talk - Rig Counts in the Middle East

In recent posts about the situation in the Middle East, I have noted the need for Aramco to increase the number of drilling rigs that it must use, since it is now looking for natural gas in their tight sand deposits rather than finding the large reserves that they had hoped in the shale reservoirs. It is interesting in this regard to plot the number of rigs that have been working in the Middle East.

Getting the overall data from Baker Hughes the rig count can be plotted, over time, to give the following:

Figure 1. Rig Counts in the Middle East (Baker Hughes)

If one looks at the trend for the last twelve months, it has remains on a fairly consistent upward trend, following that of the longer time interval plot of Figure 1.

Figure 2. Recent trend in Middle East Rig count (Baker Hughes)

Back in the days of The Oil Drum, Euan Mearns and I had this concern, which occasionally surfaced, about these numbers. From my early post on the subject which noted that back in 2005 the KSA were running around 20 rigs, which would not be enough to get them the production they were claiming to need in the future, to Euan’s in 2011, the topic was revisited regularly over the time that the count steadily mounted as the Kingdom had to drill an increasing number of wells just to keep production at around the same overall level.

I am using the KSA as the example, given the large volume of its production relative to that of the others in the Middle East, but as the numbers show, the trend toward increased drilling rate to create enough productive wells to sustain production as the larger volume wells dry up is starting to become a steadily more frantic race across the region.

Rune Likvern used the phrase “Red Queen” in discussing the overall long-term need of the companies in the Bakken to have to drill an increasing number of wells, with individually reducing production, in order to remain in place with regard to overall production. As the production from the Bakken now exceeds a million barrels a day it may seem foolish to be predicting this “squirrel cage” view of the future, but the rig count up there is still running at around 190 rigs, which is not enough to sustain future growth for long, given that access to the sweet spots is limited, and they are beginning to run out of new sites.

So it is in the Middle East. The rig count numbers are mounting steadily, it is reported that there were 88 rigs drilling in the country in October 2012. Last year this rose to 170, and the number is expected to rise to 210 by the end of this year.

Aramco have done remarkably well, over the past decade, in developing new technologies to harvest the attic oil left around the tops of the major producing formations such as Ghawar, as the main body of the fields begin to be exhausted. But the problem with these secondary rig operations is that they were directed at the smaller pools around the field, rather than tapping into the major volume, and thus they had an expected and finite life. That life is starting to come to a close. Just as, when sucking a thick milk shake through a single immovable straw, when it stops drawing fluid, there is still a fair amount left in the cup. But as you move the straw around and slide it up and down the sides, the amount that you recover gets less, and it takes greater and greater effort to get it, to the point where you quit and discard the carton. And that is where the Middle Eastern oilfields are beginning to find themselves.

The high-quality light oils of the mainland are rapidly running out, and the remaining fields with the promise for sustaining Saudi production at around 10 mbd for the next few years, are the heavier sour crudes from the offshore fields such as Safaniya and Manifa. At the same time there is a need to reduce the increasing amount of oil (now at 3 mbd) being consumed in country, with the hope that this can be replaced by domestic natural gas. But those hopes are being reduced as the shales are found to be less productive than anticipated, and hopes are now switching to the slower production that can, hopefully, be achieved from the tight sands – but at the cost of an increased number of wells, inter alia.

This is the writing on the wall for global oil production, and in the short-term it will be neglected. Increasing the number of rigs will, in that interval, increase the number of wells that will produce, even though the volume from each well will be less, and the overall life of the wells will similarly reduce, as higher production techniques tap into smaller fields.

But we are now on the treadmill in the squirrel cage, or, as Rune would have it, we have wrapped ourselves in the cape and crown of the Red Queen, and must run faster and faster just to stay in place. (There are additional concerns since, as an example, Manifa could not be brought on line until there were refineries built that could process that crude, and so the options for increasing production beyond the capacity of refineries to absorb that increase is a futile exercise).

There will soon come a time when the gain from the overall increase in new wells will not match the decline in production from older wells, particularly if the effort to “run faster” is restricted to only a few players (Russia for example is not yet putting the effort and investment into increased drilling rates in order to sustain their overall levels of production, and given the age of their major fields are likely now in terminal decline).

Ouch!

Getting the overall data from Baker Hughes the rig count can be plotted, over time, to give the following:

Figure 1. Rig Counts in the Middle East (Baker Hughes)

If one looks at the trend for the last twelve months, it has remains on a fairly consistent upward trend, following that of the longer time interval plot of Figure 1.

Figure 2. Recent trend in Middle East Rig count (Baker Hughes)

Back in the days of The Oil Drum, Euan Mearns and I had this concern, which occasionally surfaced, about these numbers. From my early post on the subject which noted that back in 2005 the KSA were running around 20 rigs, which would not be enough to get them the production they were claiming to need in the future, to Euan’s in 2011, the topic was revisited regularly over the time that the count steadily mounted as the Kingdom had to drill an increasing number of wells just to keep production at around the same overall level.

I am using the KSA as the example, given the large volume of its production relative to that of the others in the Middle East, but as the numbers show, the trend toward increased drilling rate to create enough productive wells to sustain production as the larger volume wells dry up is starting to become a steadily more frantic race across the region.

Rune Likvern used the phrase “Red Queen” in discussing the overall long-term need of the companies in the Bakken to have to drill an increasing number of wells, with individually reducing production, in order to remain in place with regard to overall production. As the production from the Bakken now exceeds a million barrels a day it may seem foolish to be predicting this “squirrel cage” view of the future, but the rig count up there is still running at around 190 rigs, which is not enough to sustain future growth for long, given that access to the sweet spots is limited, and they are beginning to run out of new sites.

So it is in the Middle East. The rig count numbers are mounting steadily, it is reported that there were 88 rigs drilling in the country in October 2012. Last year this rose to 170, and the number is expected to rise to 210 by the end of this year.

Aramco have done remarkably well, over the past decade, in developing new technologies to harvest the attic oil left around the tops of the major producing formations such as Ghawar, as the main body of the fields begin to be exhausted. But the problem with these secondary rig operations is that they were directed at the smaller pools around the field, rather than tapping into the major volume, and thus they had an expected and finite life. That life is starting to come to a close. Just as, when sucking a thick milk shake through a single immovable straw, when it stops drawing fluid, there is still a fair amount left in the cup. But as you move the straw around and slide it up and down the sides, the amount that you recover gets less, and it takes greater and greater effort to get it, to the point where you quit and discard the carton. And that is where the Middle Eastern oilfields are beginning to find themselves.

The high-quality light oils of the mainland are rapidly running out, and the remaining fields with the promise for sustaining Saudi production at around 10 mbd for the next few years, are the heavier sour crudes from the offshore fields such as Safaniya and Manifa. At the same time there is a need to reduce the increasing amount of oil (now at 3 mbd) being consumed in country, with the hope that this can be replaced by domestic natural gas. But those hopes are being reduced as the shales are found to be less productive than anticipated, and hopes are now switching to the slower production that can, hopefully, be achieved from the tight sands – but at the cost of an increased number of wells, inter alia.

This is the writing on the wall for global oil production, and in the short-term it will be neglected. Increasing the number of rigs will, in that interval, increase the number of wells that will produce, even though the volume from each well will be less, and the overall life of the wells will similarly reduce, as higher production techniques tap into smaller fields.

But we are now on the treadmill in the squirrel cage, or, as Rune would have it, we have wrapped ourselves in the cape and crown of the Red Queen, and must run faster and faster just to stay in place. (There are additional concerns since, as an example, Manifa could not be brought on line until there were refineries built that could process that crude, and so the options for increasing production beyond the capacity of refineries to absorb that increase is a futile exercise).

There will soon come a time when the gain from the overall increase in new wells will not match the decline in production from older wells, particularly if the effort to “run faster” is restricted to only a few players (Russia for example is not yet putting the effort and investment into increased drilling rates in order to sustain their overall levels of production, and given the age of their major fields are likely now in terminal decline).

Ouch!

Read more!

Sunday, July 27, 2014

Tech Talk - Changes in global supply and demand

At the beginning of the month I pointed out that there are three components to the coming Energy Mess. The first of these is the steady increase in global demand for oil and its products, the second is the decline in production from existing wells and fields, and the third is the shrinking pool of places from which new oil can be recovered to make up the difference between the first two.

Internal demand gnaws away at that available for export, as the situation in Saudi Arabia clearly illustrates:

Figure 1. Changing relation between Saudi production, internal demand and thus available exports. (Energy Export Databrowser)

Internal consumption has now reached 3 mbd – out of a production of around 10 mbd, a trend bound to go higher, as the country’s population continues to grow, having risen from 20 million in 2000 to 28.3 million in 2012, with no significant change in rate apparent.

Back in 2011 Chatham House produced a report expressing concern over the future that this prefaces. The report began with this predictive plot:

Figure 2. Projected changes in Saudi production and consumption (Chatham House )

It is regrettable to note that there is really no viable justification given for the assumption that Saudi production will rise from the current 10 mbd to the roughly 14 mbd that the plot suggests by 2020. Without that increment the world is going to be in quite a bit of hurt somewhat earlier than the above graph would suggest – as perhaps will be the Kingdom of Saudi Arabia. (Hopes for large increases in domestic production of natural gas seem to have foundered in their tight shales and are switching to efforts to develop the tight sand deposits although the mechanisms of gas flow may not be as advantageous in the sand. Similarly there is little in the report to explain why demand – once it reaches the current levels, should suddenly stabilize for three years before starting back up. Without that “hiccup” the dark blue line (which is already down to around 7 mbd, not 8) will rather continue downward, rather than the optimistic uptick that Chatham House predicted.

On the other side of the house China provides a clear example of the changes in global demand, with imports in 2013 having increased by 5.8% over 2012, and with consumption now above 10 mbd.

Figure 3. Changing relation between Chinese production, internal demand and thus necessary imports. (Energy Export Databrowser)

The other country where demand can clearly be seen to increase is India. The recent flattening of demand is likely to prove only transient, given the policies of the new government.

Figure 4. Changing relation between Indian production, internal demand and thus necessary imports. (Energy Export Databrowser)

The Indian economy has been growing at around 7% a year since 2000 and the EIA anticipates that by 2020 it will become the world’s largest oil importer, even though overall demand will not surpass China’s – which is anticipated to rise to 15.7 mbd by 2025. Although a primary focus for the new government is to give every household at least one light bulb by 2019, a significant portion of this will come from solar power. This is particularly necessary in rural areas where there is poor to no grid service. However experience in Botswana would suggest that this policy can be more difficult to achieve and sustain, given the difficulty in getting adequate maintenance outside of the cities. The Energy and Resources Institute anticipates that growth will exceed 8%. (It should be noted that the Director-General of TERI is R K Pachauri – better known for his role at the IPCC). It might further be noted that while he was still Chief Minister in Gujarat before the election, the new Indian Prime Minister had raised the GDP of that state to an average of 13.4% in comparison with the national rate of 7.8%.

To a degree this problem of imbalance in the supply:demand situation that will develop in the next couple of years will be rectified by a change in the price structure of oil. Tightening of supply against even current levels of supply (let alone that needed to meet the July 2014 OPEC MOMR estimate of a continued growth in demand of the order of 1.16 mbd) will lead to an increase in price. It is that cost increase that will most likely impact countries such as India, who have, in the past, been bid out of a number of foreign oil investments by China, and who are likely to see that situation continue, of not get worse.

The presumption that Russia will be able to help China by exporting more oil East, while sustaining its exports to the West, is likely an unrealistic projection. Russia is already seeing their overall export levels decline, even before production itself significantly falls off, and the combination will tighten the market in the near future.

Figure 5. Changing relation between Russian production, internal demand and thus exports. (Energy Export Databrowser)

China is currently seeing an ongoing internal fight over the China National Petroleum Corporation (CNPC). Jiang Jiemin has been arrested and the investigation is progressing down his chain of command and influence.

An increase in the price of oil, just as the links to foreign suppliers become questioned through this internal investigation that may spread beyond China, may weaken those links and give countries such as India an opportunity to achieve supplies that might otherwise be more difficult to achieve.

Internal demand gnaws away at that available for export, as the situation in Saudi Arabia clearly illustrates:

Figure 1. Changing relation between Saudi production, internal demand and thus available exports. (Energy Export Databrowser)

Internal consumption has now reached 3 mbd – out of a production of around 10 mbd, a trend bound to go higher, as the country’s population continues to grow, having risen from 20 million in 2000 to 28.3 million in 2012, with no significant change in rate apparent.

Back in 2011 Chatham House produced a report expressing concern over the future that this prefaces. The report began with this predictive plot:

Figure 2. Projected changes in Saudi production and consumption (Chatham House )

It is regrettable to note that there is really no viable justification given for the assumption that Saudi production will rise from the current 10 mbd to the roughly 14 mbd that the plot suggests by 2020. Without that increment the world is going to be in quite a bit of hurt somewhat earlier than the above graph would suggest – as perhaps will be the Kingdom of Saudi Arabia. (Hopes for large increases in domestic production of natural gas seem to have foundered in their tight shales and are switching to efforts to develop the tight sand deposits although the mechanisms of gas flow may not be as advantageous in the sand. Similarly there is little in the report to explain why demand – once it reaches the current levels, should suddenly stabilize for three years before starting back up. Without that “hiccup” the dark blue line (which is already down to around 7 mbd, not 8) will rather continue downward, rather than the optimistic uptick that Chatham House predicted.

On the other side of the house China provides a clear example of the changes in global demand, with imports in 2013 having increased by 5.8% over 2012, and with consumption now above 10 mbd.

Figure 3. Changing relation between Chinese production, internal demand and thus necessary imports. (Energy Export Databrowser)

The other country where demand can clearly be seen to increase is India. The recent flattening of demand is likely to prove only transient, given the policies of the new government.

Figure 4. Changing relation between Indian production, internal demand and thus necessary imports. (Energy Export Databrowser)

The Indian economy has been growing at around 7% a year since 2000 and the EIA anticipates that by 2020 it will become the world’s largest oil importer, even though overall demand will not surpass China’s – which is anticipated to rise to 15.7 mbd by 2025. Although a primary focus for the new government is to give every household at least one light bulb by 2019, a significant portion of this will come from solar power. This is particularly necessary in rural areas where there is poor to no grid service. However experience in Botswana would suggest that this policy can be more difficult to achieve and sustain, given the difficulty in getting adequate maintenance outside of the cities. The Energy and Resources Institute anticipates that growth will exceed 8%. (It should be noted that the Director-General of TERI is R K Pachauri – better known for his role at the IPCC). It might further be noted that while he was still Chief Minister in Gujarat before the election, the new Indian Prime Minister had raised the GDP of that state to an average of 13.4% in comparison with the national rate of 7.8%.

To a degree this problem of imbalance in the supply:demand situation that will develop in the next couple of years will be rectified by a change in the price structure of oil. Tightening of supply against even current levels of supply (let alone that needed to meet the July 2014 OPEC MOMR estimate of a continued growth in demand of the order of 1.16 mbd) will lead to an increase in price. It is that cost increase that will most likely impact countries such as India, who have, in the past, been bid out of a number of foreign oil investments by China, and who are likely to see that situation continue, of not get worse.

The presumption that Russia will be able to help China by exporting more oil East, while sustaining its exports to the West, is likely an unrealistic projection. Russia is already seeing their overall export levels decline, even before production itself significantly falls off, and the combination will tighten the market in the near future.

Figure 5. Changing relation between Russian production, internal demand and thus exports. (Energy Export Databrowser)

China is currently seeing an ongoing internal fight over the China National Petroleum Corporation (CNPC). Jiang Jiemin has been arrested and the investigation is progressing down his chain of command and influence.

CNPC is one of the world's largest companies, with global operations and 2013 revenue of $432 billion. Its publicly listed subsidiary, PetroChina, trades in Hong Kong, Shanghai and New York and is the world's fourth-biggest oil producer by market capitalization. Jiang ran both the parent and PetroChina from 2007 until last year, when he briefly headed the State-Owned Assets Supervision and Administration Commission (SASAC).The arrests and investigations will likely slow the rate of Chinese investment in the foreign energy market, but is not likely to have any impact on internal energy consumption. Rather it may make it more difficult for China to sustain their necessary supply of oil as times become more troubled.

The investigation has already touched CNPC group operations in Canada, Indonesia, China and Turkmenistan, say people familiar with the proceedings. In addition to Jiang, the Chinese authorities have confirmed the arrests of CNPC vice president Wang Yongchun, PetroChina vice presidents Li Hualin and Ran Xinquan, and the listed unit's chief geologist, Wang Daofu.

An increase in the price of oil, just as the links to foreign suppliers become questioned through this internal investigation that may spread beyond China, may weaken those links and give countries such as India an opportunity to achieve supplies that might otherwise be more difficult to achieve.

Read more!

Wednesday, May 7, 2014

Tech Talk - Fast destruction and slow reconstruction

Underlying many of the projections of future energy supply that are now being made there are, as mentioned earlier, a lot of assumptions that are beginning to appear more questionable as time passes. Much of the concern has to focus on the instability in the Middle East and North African nations (MENA) that are now increasingly unsettled by civil conflict. While optimism in many reviews anticipates that the turmoil will decline and nations will return to pre-conflict levels or higher, particularly in the case of Iraq, unfortunately this conflicts with much of what we have learned from recent history. Sadly there is also the history of Gazprom, which now also suggests that rosy visions of the future are only that, and what is coming is likely to be much grimmer.

Considering first Libya, once the infrastructure of an oilfield and its links to the outside world, and the operators that run it have been destroyed, seriously damaged or dissuaded from being there, then, particularly where conflict continues over time, restoration of pre-conflict volumes can take more than a decade. Once combatants become embittered by the realities of civil war, so their willingness to subsume the hatreds and other burdens brought on by loss becomes more difficult to engage, and conflict drags on with its continued losses for society. Libya is a sad example of how rapidly production can collapse.

Figure 1. Libyan oil production pre-current conflict (SEPM strata )

The country has now reached as low a rate of daily production (around 240 kbd) as it has seen in recent years.

Figure 2. Recent Libyan oil production (from OPEC MOMR)

For some time the powers that be have continued to hope and even project that Libyan production can return to levels of around a million bd, but those hopes seem dubious at best.

Just a week ago the National Oil Corporation announced that it was lifting the “Force Majeure” designation for the Oil Harbor at Zuetina. The first tanker was to load on Friday. According to a Bloomberg report the Ottoman Tenacity was to pick up a cargo of 600,000 barrels from Zuetina and carry it to Europe. The ship was reported to be loading on Friday and is currently just off Cagliari in Sardinia.

Figure 3. Location of the Ottoman Tenacity on Wed May 7th (Marine Traffic )

A second ship was supposedly loading up to 850,000 barrels at Haringa destined for France. Yet according to Marine Traffic it is now (Wednesday) off the coast of Tunisia, and does not, in the end, appear to have revisited Haringa.

The situation in Libya is not really stable, despite the hopes. On Sunday the Parliament swore in a new Prime Minister but his support is not strong, and factions continue to challenge his election. Attacks on the military are also on the increase. Meanwhile the blockade of the Sharara oilfield continues. It is hard to see oil production increasing much above the current levels, despite the optimism.

Yet if this effectively has removed a million bd from the global market, where can this be made up? In the short term Saudi Arabia increased production to cover the shortfall, and is still producing around 9.7 mbd. OPEC production overall remains at around 30 mbd, and is projected to remain at this level over the year.

OPEC notes that the Former Soviet Union is expected to increase production by around 200,000 bd this year, of which almost half will come from Russia itself, but OPEC are careful to include a word of caution in their predictions of Russian output.

Gazprom has, in the past, shown that it can, when necessary, play hard ball to ensure that it owns and controls the market for natural gas (just ask BP or Turkmenistan), and with the demise of the Nabucco pipeline is in increasing control of natural gas supplies into Europe. That condition cannot change in the short term, LNG facilities take years to plan, permit and construct, and thus the control which Russia exerts over Europe through this grip on the various supply pipelines is likely to continue to influence European opinion and, more realistically, actions in the next few years.

What this all means for the future of Ukraine is rather unfortunate – regrettably it is not clear that Russian ambition will end there and one would suspect that, given the limitations in response to the current and earlier (Georgia) Russian activity, that it will not. How this will affect overall oil and natural gas supply is unclear. OPEC concerns over future Russian production levels appear justified, especially since future developments in Russia will require increasing levels of capital, which might instead be directed at supporting Russian foreign policies – reducing overall volumes available, and more particularly the volumes that Europe has come to depend on. It could make for a couple of interesting years, since there are few alternatives that can be developed within that time frame. And certainly there is, at present, little will to make the capital investments that might bring them about.

Sadly history suggests that the outcome will not be a good one, there are few precedents that would show how one might get out of the increasing messes caused by political instability.

Considering first Libya, once the infrastructure of an oilfield and its links to the outside world, and the operators that run it have been destroyed, seriously damaged or dissuaded from being there, then, particularly where conflict continues over time, restoration of pre-conflict volumes can take more than a decade. Once combatants become embittered by the realities of civil war, so their willingness to subsume the hatreds and other burdens brought on by loss becomes more difficult to engage, and conflict drags on with its continued losses for society. Libya is a sad example of how rapidly production can collapse.

Figure 1. Libyan oil production pre-current conflict (SEPM strata )

The country has now reached as low a rate of daily production (around 240 kbd) as it has seen in recent years.

Figure 2. Recent Libyan oil production (from OPEC MOMR)

For some time the powers that be have continued to hope and even project that Libyan production can return to levels of around a million bd, but those hopes seem dubious at best.

Just a week ago the National Oil Corporation announced that it was lifting the “Force Majeure” designation for the Oil Harbor at Zuetina. The first tanker was to load on Friday. According to a Bloomberg report the Ottoman Tenacity was to pick up a cargo of 600,000 barrels from Zuetina and carry it to Europe. The ship was reported to be loading on Friday and is currently just off Cagliari in Sardinia.

Figure 3. Location of the Ottoman Tenacity on Wed May 7th (Marine Traffic )

A second ship was supposedly loading up to 850,000 barrels at Haringa destined for France. Yet according to Marine Traffic it is now (Wednesday) off the coast of Tunisia, and does not, in the end, appear to have revisited Haringa.

The situation in Libya is not really stable, despite the hopes. On Sunday the Parliament swore in a new Prime Minister but his support is not strong, and factions continue to challenge his election. Attacks on the military are also on the increase. Meanwhile the blockade of the Sharara oilfield continues. It is hard to see oil production increasing much above the current levels, despite the optimism.

Yet if this effectively has removed a million bd from the global market, where can this be made up? In the short term Saudi Arabia increased production to cover the shortfall, and is still producing around 9.7 mbd. OPEC production overall remains at around 30 mbd, and is projected to remain at this level over the year.

OPEC notes that the Former Soviet Union is expected to increase production by around 200,000 bd this year, of which almost half will come from Russia itself, but OPEC are careful to include a word of caution in their predictions of Russian output.

The risk to Russia’s supply forecast remains high on technical, political and natural decline grounds.It is the increasing political risks associated with Russian production, and the supply of that fuel to Europe that are perhaps of most concern. An article in Der Speigel points out that the Russian grip on German fuel supplies is only increasing. One of the Russian oligarchs has just bought one of the German oil and gas production companies for $7.1 billion, and now controls a fifth of German natural gas production and a quarter of its oil production. Another fifth of the German natural gas market, provided by Wingas, is also now Russian as Gazprom bought the company, and its distribution network, in a sale to be finalized this summer. And while Europe is seeing more LNG receiving facilities being constructed there is still a global shortage of export facilities to match that demand. As a result current facilities are significantly under-utilized.

Gazprom has, in the past, shown that it can, when necessary, play hard ball to ensure that it owns and controls the market for natural gas (just ask BP or Turkmenistan), and with the demise of the Nabucco pipeline is in increasing control of natural gas supplies into Europe. That condition cannot change in the short term, LNG facilities take years to plan, permit and construct, and thus the control which Russia exerts over Europe through this grip on the various supply pipelines is likely to continue to influence European opinion and, more realistically, actions in the next few years.

What this all means for the future of Ukraine is rather unfortunate – regrettably it is not clear that Russian ambition will end there and one would suspect that, given the limitations in response to the current and earlier (Georgia) Russian activity, that it will not. How this will affect overall oil and natural gas supply is unclear. OPEC concerns over future Russian production levels appear justified, especially since future developments in Russia will require increasing levels of capital, which might instead be directed at supporting Russian foreign policies – reducing overall volumes available, and more particularly the volumes that Europe has come to depend on. It could make for a couple of interesting years, since there are few alternatives that can be developed within that time frame. And certainly there is, at present, little will to make the capital investments that might bring them about.

Sadly history suggests that the outcome will not be a good one, there are few precedents that would show how one might get out of the increasing messes caused by political instability.

Read more!

Sunday, August 11, 2013

Tech Talk - Oil Supply, Oil Prices and the Kingdom of Saudi Arabia

From the time that The Oil Drum first began, and through the years up to the Recession of 2008-9 there was an increase in the price of oil, and that resumed following the initial period of that recession, and, in contrast to the price of natural gas, oil has recovered a lot of the price that it lost.

Figure 1. Comparable price of oil from 1946 (Inflation data)

And if one were to draw a straight line on that graph from the low point in 1999 though now there hasn’t been a huge variation away from the slope of that line for long. That, of course, does not stop folk from pointing to the very short, roughly flat, bit at the end and saying that oil prices are going to remain at that level, or are even about to decline.

To address that final point first, I would suggest that those making such a foolish prediction should go away and read the OPEC Monthly Oil Market Reports. Remember that, for just a little while longer, oil is a fungible product. OPEC make no secret of the fact that they continuously examine the global economy and make estimates on how it is going to behave. This month they note that the economies aren’t doing quite as well as expected, and have revised down global growth to 2.9%, though they expect next year to be better, and hold to their estimate of a 3.5% growth rate.

But OPEC go beyond just making that prediction, they use it, and data that they have on consumption and oil supplies around the world, to estimate how much OPEC should produce each month to balance supply against demand, so that the price will remain at a comfortable level for the OPEC economies. And based on those numbers they tailor production.

This month, for example, they note that global oil demand is anticipated to grow by 0.8 mbd this year (and by 1.04 mbd in 2014). They anticipate growth in production of around 1.0 mbd from the non-OPEC nations, with projected increases from Canada, the United States, Brazil, the Sudans and Kazakhstan contributing to an additional 1.1 mbd next year. From these numbers they can project that demand for OPEC oil will be slightly down this year, at 29.9 mbd down 0.4 mbd on last year, with next year seeing an additional fall of 0.3 mbd on average.

Figure 2. Projected oil demand for 2013 (OPEC MOMR )

Thus slight reductions in production from OPEC, and particularly the Kingdom of Saudi Arabia, (KSA) can keep the world supply in balance with demand and more critically for them keep the price up at a level that they are comfortable with. Note that in relation to the overall volumes of oil being traded they are not talking much adjustment in their overall volume (around 1% of the total 30 mbd) in order to sustain prices. The USA produces more, OPEC produces less – not much less because global demand is growing – and the price is sustained.

This has virtually nothing to do with the speculators on Wall Street and the corrections they might impose, this is all about supplying a needed volume to meet a demand and controlling that supply to ensure that the price is sustained.

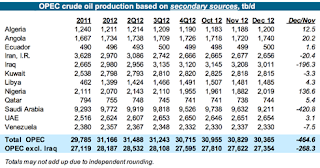

There are a number of caveats to this simplified explanation, one being the short-term willingness and ability of some producers to keep to their targets. One of the imponderables is the production from Iraq. Although Iraq has been given a waiver through 2014 on the need to limit their production, the increasing violence has led to a drop in production, back below 3 mbd.

Figure 3. OPEC production based on data from secondary sources (OPEC MOMR)

As I have noted in the past, OPEC is sufficiently suspicious of the reported numbers from the countries themselves that they check from secondary sources, and provide both sets of numbers.

Figure 4. OPEC production numbers from the originating countries. (OPEC MOMR August 2013)

Note, for example, that Iran says that it is producing over 1 mbd more than other sources report, and Venezuela is around 400 kbd light. The balancing act is largely the charge of KSA, since it produces the largest amount and can adjust more readily to balance the need.

One of the other caveats is that the internal demand in these countries is rising, and that lowers the amount that can be exported. This will in time require that OPEC produce more, just to sustain the amounts that they export. And the problem here is the biggest caveat of all. Because KSA cannot continue to produce ever increasing amounts of oil.

Just exactly how much the country can produce is the subject of much debate, and has been at The Oil Drum since its inception. But if I can now gently admonish those who think it can keep increasing forever, and that it has vast reserves that can flood the market at need. This fails to recognize that the major fields on which the country has relied are no longer capable of their historic production levels, and that, over the time that TOD has been in existence, production has switched to the new fields that KSA had promised it would, back in time.

But these new fields, including Manifa and Safaniya produce a heavier crude that, for years, KSA struggled, usually in vain, to find a market for internationally. It is only now that it is building its own refineries to process the oil that it can find a global market for the product. Yet those refineries have only a limited capacity. If you can’t ship, refine and market your product in the form that the customer needs, it can’t be sold, regardless of how much, instantaneously, you can pump out of the ground. And so KSA is starting to look harder for other fields. They have increased the number of rigs employed to 170 by the end of the year (in 2005 they had about 20 oil and 10 gas rigs operating), going beyond the 160 estimated earlier, seeking both to raise production from existing fields, but also to find new ones. This is almost double the number that Euan reported at the end of last year. That this is being expedited is not good news! Because new fields will very likely be smaller, and more rapidly exhausted, and may not have the quality of the oil produced from Ghawar and the other old faithfuls.

Realistically, over a couple of years, I would suspect that the oil price line, that I mentioned was rising at the beginning of the piece will continue to rise and we are just going to have to accommodate to it.

Figure 1. Comparable price of oil from 1946 (Inflation data)

And if one were to draw a straight line on that graph from the low point in 1999 though now there hasn’t been a huge variation away from the slope of that line for long. That, of course, does not stop folk from pointing to the very short, roughly flat, bit at the end and saying that oil prices are going to remain at that level, or are even about to decline.

To address that final point first, I would suggest that those making such a foolish prediction should go away and read the OPEC Monthly Oil Market Reports. Remember that, for just a little while longer, oil is a fungible product. OPEC make no secret of the fact that they continuously examine the global economy and make estimates on how it is going to behave. This month they note that the economies aren’t doing quite as well as expected, and have revised down global growth to 2.9%, though they expect next year to be better, and hold to their estimate of a 3.5% growth rate.

But OPEC go beyond just making that prediction, they use it, and data that they have on consumption and oil supplies around the world, to estimate how much OPEC should produce each month to balance supply against demand, so that the price will remain at a comfortable level for the OPEC economies. And based on those numbers they tailor production.

This month, for example, they note that global oil demand is anticipated to grow by 0.8 mbd this year (and by 1.04 mbd in 2014). They anticipate growth in production of around 1.0 mbd from the non-OPEC nations, with projected increases from Canada, the United States, Brazil, the Sudans and Kazakhstan contributing to an additional 1.1 mbd next year. From these numbers they can project that demand for OPEC oil will be slightly down this year, at 29.9 mbd down 0.4 mbd on last year, with next year seeing an additional fall of 0.3 mbd on average.

Figure 2. Projected oil demand for 2013 (OPEC MOMR )

Thus slight reductions in production from OPEC, and particularly the Kingdom of Saudi Arabia, (KSA) can keep the world supply in balance with demand and more critically for them keep the price up at a level that they are comfortable with. Note that in relation to the overall volumes of oil being traded they are not talking much adjustment in their overall volume (around 1% of the total 30 mbd) in order to sustain prices. The USA produces more, OPEC produces less – not much less because global demand is growing – and the price is sustained.

This has virtually nothing to do with the speculators on Wall Street and the corrections they might impose, this is all about supplying a needed volume to meet a demand and controlling that supply to ensure that the price is sustained.

There are a number of caveats to this simplified explanation, one being the short-term willingness and ability of some producers to keep to their targets. One of the imponderables is the production from Iraq. Although Iraq has been given a waiver through 2014 on the need to limit their production, the increasing violence has led to a drop in production, back below 3 mbd.

Figure 3. OPEC production based on data from secondary sources (OPEC MOMR)

As I have noted in the past, OPEC is sufficiently suspicious of the reported numbers from the countries themselves that they check from secondary sources, and provide both sets of numbers.

Figure 4. OPEC production numbers from the originating countries. (OPEC MOMR August 2013)

Note, for example, that Iran says that it is producing over 1 mbd more than other sources report, and Venezuela is around 400 kbd light. The balancing act is largely the charge of KSA, since it produces the largest amount and can adjust more readily to balance the need.

One of the other caveats is that the internal demand in these countries is rising, and that lowers the amount that can be exported. This will in time require that OPEC produce more, just to sustain the amounts that they export. And the problem here is the biggest caveat of all. Because KSA cannot continue to produce ever increasing amounts of oil.

Just exactly how much the country can produce is the subject of much debate, and has been at The Oil Drum since its inception. But if I can now gently admonish those who think it can keep increasing forever, and that it has vast reserves that can flood the market at need. This fails to recognize that the major fields on which the country has relied are no longer capable of their historic production levels, and that, over the time that TOD has been in existence, production has switched to the new fields that KSA had promised it would, back in time.

But these new fields, including Manifa and Safaniya produce a heavier crude that, for years, KSA struggled, usually in vain, to find a market for internationally. It is only now that it is building its own refineries to process the oil that it can find a global market for the product. Yet those refineries have only a limited capacity. If you can’t ship, refine and market your product in the form that the customer needs, it can’t be sold, regardless of how much, instantaneously, you can pump out of the ground. And so KSA is starting to look harder for other fields. They have increased the number of rigs employed to 170 by the end of the year (in 2005 they had about 20 oil and 10 gas rigs operating), going beyond the 160 estimated earlier, seeking both to raise production from existing fields, but also to find new ones. This is almost double the number that Euan reported at the end of last year. That this is being expedited is not good news! Because new fields will very likely be smaller, and more rapidly exhausted, and may not have the quality of the oil produced from Ghawar and the other old faithfuls.

Realistically, over a couple of years, I would suspect that the oil price line, that I mentioned was rising at the beginning of the piece will continue to rise and we are just going to have to accommodate to it.

Read more!

Thursday, July 18, 2013

To Forbes - A Gentle Cough of Correction at TOD's end

Forbes recently issued a commentary on the closing of The Oil Drum, which deserves some rebuttal, since, as with many stories on the "Peak Oil" topic, it conveys too many incorrect statements and false assumptions.

Just over eight years ago I became irritated by several articles in the Main Stream Media that were clearly technically wrong. (My academic research includes many years of making holes in geological media, an interest that began with my doctoral work in the late 1960’s). I began writing about some of the misconceptions in regard to the approach of Peak Oil in a blog I was writing at the time. Shortly thereafter I agreed to join with Kyle, who was then writing his own blog, under the nom de plume of Prof Goose, to jointly create the website The Oil Drum.

In the beginning, Kyle handled the site management issues (a task he later passed on), and my main contribution has been the intended one of writing on the more technical sides of the situation. This was particularly the case during the events surrounding the Deepwater Horizon disaster, where readership of TOD rose to around 60,000 a day. But writing to a site that began to achieve some technical credibility had its drawbacks. Very early on I got into the habit of referencing almost every fact I cited, given the questions that arose whenever I appeared (at least to my audience, but also, at times, in fact) to misspeak. Working for the site has made me a better writer, but it was clear almost from the start that the two of us could not sustain the interest that the site very quickly drew.

Over the years I felt very fortunate that Kyle went out and found funding, and innocents willing to carry the burden of editing the increasingly large talent of folk that were kind enough to contribute to the large interest that the site engendered. The site was fortunate to attract some really perceptive folk, and if I hesitate to name them it is only from the fear of missing the odd one and causing offence to people that I have acquired great respect for over the years. Many of those now have their own sites, and so TOD acted in some small way as an encouragement for that effort and to broaden and grow the community that is concerned about the coming point where the production of oil, at a reasonable price, will be unable to keep up with demand and the unpleasant consequences that will then arrive.

I was watching the hearing before the UK House of Commons Science and Technology Committee this past Wednesday on the public understanding of climate. In response to a question, Ralph Lee of Factual, Channel 4 and David Jordan, Director of Editorial Policy and Standards for the BBC pointed out the difficulty in sustaining the level of stories on Climate Change, because of the need for these to generate significant new material to justify publication. They noted that repetition of the basic information, beyond a certain point, was counter-productive. So it is with the Peak Oil story. The facts, in neither case, change, but the amount of new information while accumulating (vide the superb work that Leanan has done with Drumbeat over the years) is often repetitive or confirmatory of earlier stories and thus harder to turn into interesting and exciting new material. There are developing stories that justify continued interest in the topic, but the slow pace with which some of the stories unfold make it difficult to sustain interest.

The transition of Egypt to an importing state for example, revealed in the Energy Export Databrowser figure shown a few weeks ago illustrates a growing problem that their new government must address, but it can only be covered a few times before interest wanes.

Figure 1. Change in oil consumption and the need for more imports for Egypt (Energy Export Databrowser)

And this holds true for many of the topics covered in the past years. The perceptive articles written at TOD on Saudi Arabia by Stuart Staniford (who now writes Early Warning), Euan Mearns and with JoulesBurn’s images from the satellites showed how Ghawar was in significant decline. But there are only so many photos of oil rig sites in the desert that can be made interesting. Aramco are switching to the heavier oils offshore. Manifa has just started new production and Safaniya is being expanded. These are needed to offset the permanent declines in production from the older fields, but again, other than chronicling these steps it is hard to sustain interest in an inexorable process that takes years to play out and where the route to Peak Oil is following along many of the predicted lines.

Even drawing back the curtains of hype over the Bakken and Eagle Ford production, which Rune and Art have so ably done, can only be written about at a certain low frequency before folk see it as repetitious.

Much of the story of the future supply will, in my view, come from activity outside the United States. There will always be a need to update activities in and offshore Alaska, and in the US shales and other formations where future production will have to come from, but as we are likely to see by the end of this year, the gilt on that gingerbread is very thin. Thus the posts that I have been writing recently (and which will continue on Bit Tooth Energy – my own home site) will likely focus on the situations abroad, such as the Middle East, where the political upheaval has a much greater potential to disturb overall global supply than the changes in the US. Similarly Japan is moving toward a more militant attitude as China moves to extract fuel from disputed fields in the East China Sea. This however, again, is a potential tragedy unfolding in slow motion.

At the beginning of the year the EIA were predicting that gas prices would fall this year and pundits that suggested that gas prices would stay down after the recession still appear with regularity to quote their lines of optimism, even as gas prices stay stubbornly high and potentially may rise through the rest of the year. Why is that? Well the OPEC nations need a certain level of income and adjust their production each month to help sustain prices – something these optimists seem unwilling to recognize.

The problem, however, is that if global demand rises at (for the sake of discussion) 1 mbd a year, then a point will be reached, fairly soon when increasingly this OPEC supply becomes no longer capable of filling the demand. Prices will then rise again, balancing supply against those able to pay for their demand at that price. Stating that this is not going to happen because "a way will be found" is to remain an ostrich.

No, gentle readers, the closing of TOD is, in my opinion, based on a deliberate but IMHO faulty management decision made in that group a couple of years ago. It was predictable at that time, but it has nothing to do with the coming of Peak Oil, and is not even symptomatic of much of a delay in that arrival.

And with that off my chest I will return to writing about the evolving problems. My hope at the founding of TOD was that it would chronicle the events through the Peak, it got to nearly the Peak, though I don’t anticipate that this will be a pleasant story beyond that point. But, that coverage will now shift to being only at a new location at a time chosen by the TOD editors.

Just over eight years ago I became irritated by several articles in the Main Stream Media that were clearly technically wrong. (My academic research includes many years of making holes in geological media, an interest that began with my doctoral work in the late 1960’s). I began writing about some of the misconceptions in regard to the approach of Peak Oil in a blog I was writing at the time. Shortly thereafter I agreed to join with Kyle, who was then writing his own blog, under the nom de plume of Prof Goose, to jointly create the website The Oil Drum.

In the beginning, Kyle handled the site management issues (a task he later passed on), and my main contribution has been the intended one of writing on the more technical sides of the situation. This was particularly the case during the events surrounding the Deepwater Horizon disaster, where readership of TOD rose to around 60,000 a day. But writing to a site that began to achieve some technical credibility had its drawbacks. Very early on I got into the habit of referencing almost every fact I cited, given the questions that arose whenever I appeared (at least to my audience, but also, at times, in fact) to misspeak. Working for the site has made me a better writer, but it was clear almost from the start that the two of us could not sustain the interest that the site very quickly drew.

Over the years I felt very fortunate that Kyle went out and found funding, and innocents willing to carry the burden of editing the increasingly large talent of folk that were kind enough to contribute to the large interest that the site engendered. The site was fortunate to attract some really perceptive folk, and if I hesitate to name them it is only from the fear of missing the odd one and causing offence to people that I have acquired great respect for over the years. Many of those now have their own sites, and so TOD acted in some small way as an encouragement for that effort and to broaden and grow the community that is concerned about the coming point where the production of oil, at a reasonable price, will be unable to keep up with demand and the unpleasant consequences that will then arrive.

I was watching the hearing before the UK House of Commons Science and Technology Committee this past Wednesday on the public understanding of climate. In response to a question, Ralph Lee of Factual, Channel 4 and David Jordan, Director of Editorial Policy and Standards for the BBC pointed out the difficulty in sustaining the level of stories on Climate Change, because of the need for these to generate significant new material to justify publication. They noted that repetition of the basic information, beyond a certain point, was counter-productive. So it is with the Peak Oil story. The facts, in neither case, change, but the amount of new information while accumulating (vide the superb work that Leanan has done with Drumbeat over the years) is often repetitive or confirmatory of earlier stories and thus harder to turn into interesting and exciting new material. There are developing stories that justify continued interest in the topic, but the slow pace with which some of the stories unfold make it difficult to sustain interest.

The transition of Egypt to an importing state for example, revealed in the Energy Export Databrowser figure shown a few weeks ago illustrates a growing problem that their new government must address, but it can only be covered a few times before interest wanes.

Figure 1. Change in oil consumption and the need for more imports for Egypt (Energy Export Databrowser)

And this holds true for many of the topics covered in the past years. The perceptive articles written at TOD on Saudi Arabia by Stuart Staniford (who now writes Early Warning), Euan Mearns and with JoulesBurn’s images from the satellites showed how Ghawar was in significant decline. But there are only so many photos of oil rig sites in the desert that can be made interesting. Aramco are switching to the heavier oils offshore. Manifa has just started new production and Safaniya is being expanded. These are needed to offset the permanent declines in production from the older fields, but again, other than chronicling these steps it is hard to sustain interest in an inexorable process that takes years to play out and where the route to Peak Oil is following along many of the predicted lines.

Even drawing back the curtains of hype over the Bakken and Eagle Ford production, which Rune and Art have so ably done, can only be written about at a certain low frequency before folk see it as repetitious.

Much of the story of the future supply will, in my view, come from activity outside the United States. There will always be a need to update activities in and offshore Alaska, and in the US shales and other formations where future production will have to come from, but as we are likely to see by the end of this year, the gilt on that gingerbread is very thin. Thus the posts that I have been writing recently (and which will continue on Bit Tooth Energy – my own home site) will likely focus on the situations abroad, such as the Middle East, where the political upheaval has a much greater potential to disturb overall global supply than the changes in the US. Similarly Japan is moving toward a more militant attitude as China moves to extract fuel from disputed fields in the East China Sea. This however, again, is a potential tragedy unfolding in slow motion.

At the beginning of the year the EIA were predicting that gas prices would fall this year and pundits that suggested that gas prices would stay down after the recession still appear with regularity to quote their lines of optimism, even as gas prices stay stubbornly high and potentially may rise through the rest of the year. Why is that? Well the OPEC nations need a certain level of income and adjust their production each month to help sustain prices – something these optimists seem unwilling to recognize.

The problem, however, is that if global demand rises at (for the sake of discussion) 1 mbd a year, then a point will be reached, fairly soon when increasingly this OPEC supply becomes no longer capable of filling the demand. Prices will then rise again, balancing supply against those able to pay for their demand at that price. Stating that this is not going to happen because "a way will be found" is to remain an ostrich.

No, gentle readers, the closing of TOD is, in my opinion, based on a deliberate but IMHO faulty management decision made in that group a couple of years ago. It was predictable at that time, but it has nothing to do with the coming of Peak Oil, and is not even symptomatic of much of a delay in that arrival.

And with that off my chest I will return to writing about the evolving problems. My hope at the founding of TOD was that it would chronicle the events through the Peak, it got to nearly the Peak, though I don’t anticipate that this will be a pleasant story beyond that point. But, that coverage will now shift to being only at a new location at a time chosen by the TOD editors.

Read more!

Thursday, April 25, 2013

OGPSS - OPEC and EIA short term projections

Just this month Saudi Aramco announced that production had begun at their Manifa oilfield, and by July would be supplying up to 500 kbd to the new refinery that is being built at Jamail with the collaboration of Total. The first oil from the refinery is expected to ship in August, and both projects are currently ahead of schedule. Manifa will further increase in production next year, to 900 kbd, with the additional flow going to the Yanbu refinery being built with the collaboration of Sinopec. Both these refineries are designed to take heavy crude, and can also accept oil from the ongoing projects to expand production at Safaniya. Collectively this is said to ensure that the company will be able to achieve a maximum sustainable production of 12 mbd.